Special Report: State of the Profession Report 2017

Digital tools and smart technologies spark a new era in manufacturing.

Automotive assembly lines continue to pace the manufacturing world. Photo courtesy Toyota Motor Corp.

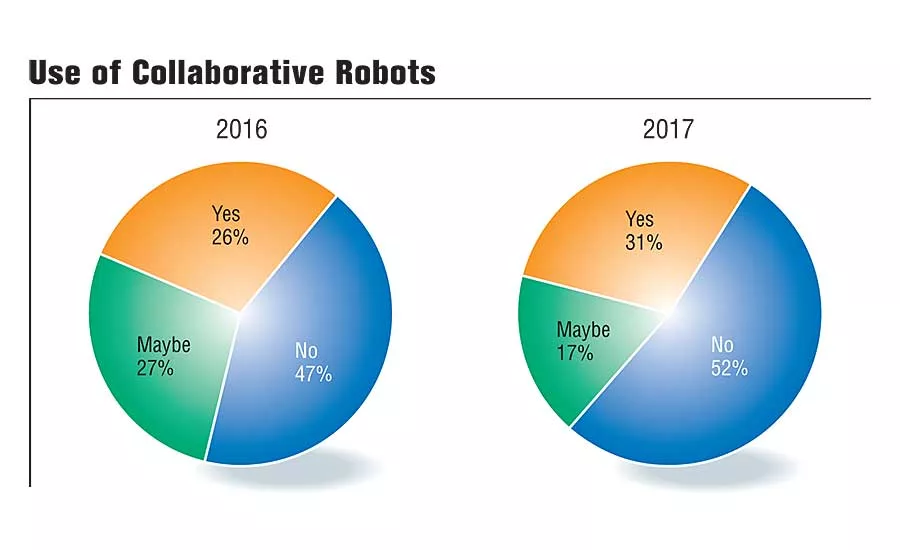

Use of Collaborative Robots

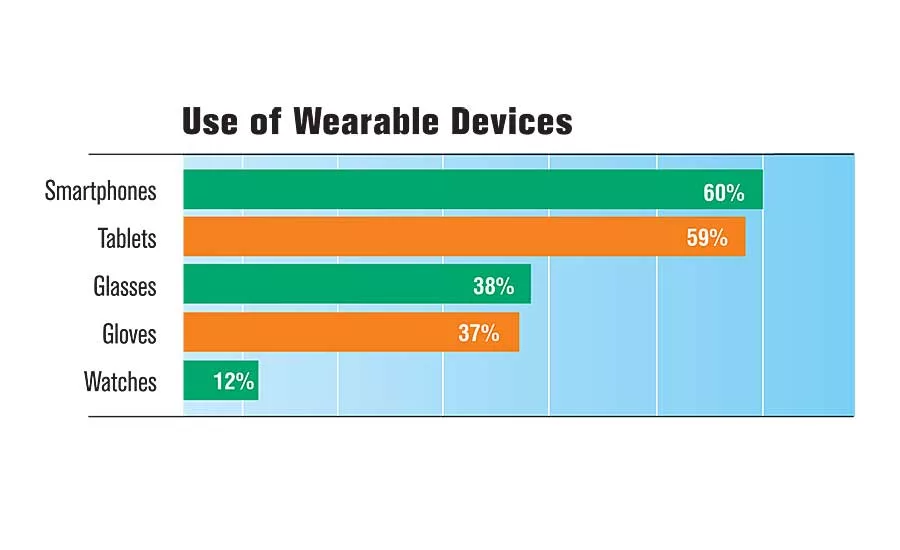

Use of Wearable Devices

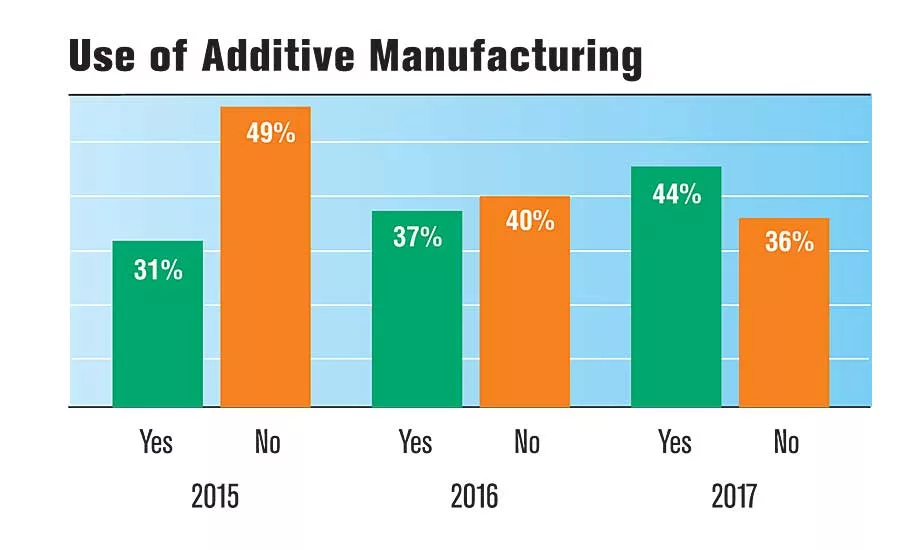

Use of Additive Manufacturing

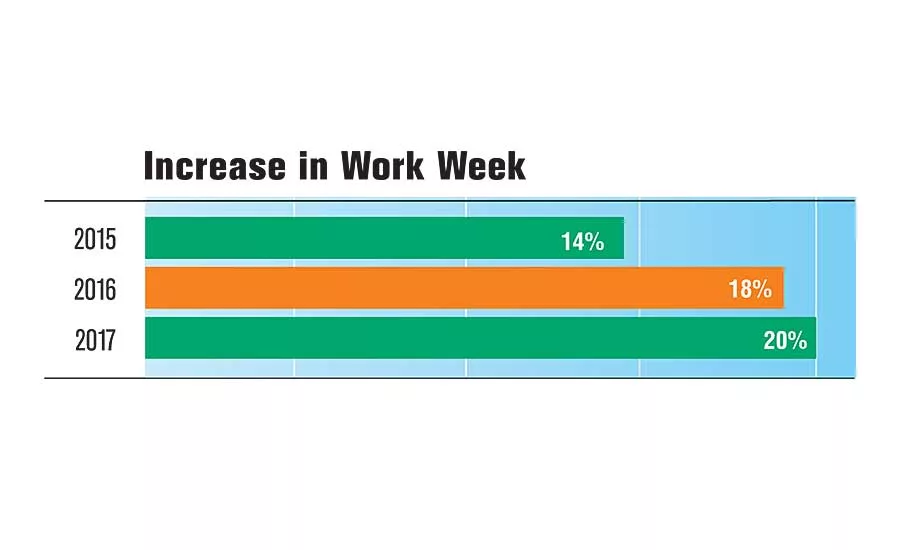

Increase in Work Week

How Industries Compare

Geography Affects Compensation

Factors Contributing to Competitive Advantage

Reshoring of Assembly Operations

Time to Fill Skilled Positions

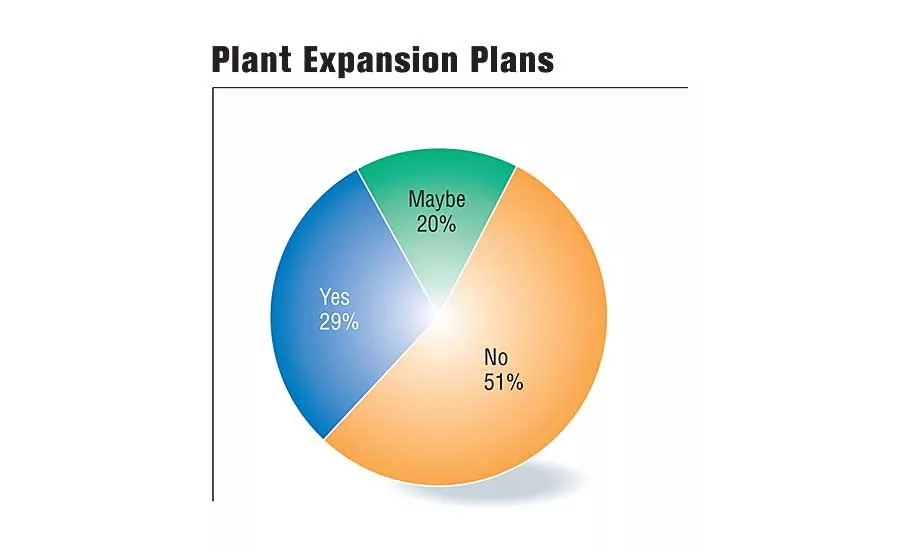

Plant Expansion Plans

The era of digital manufacturing, Industry 4.0 and smart factories is here. It promises to improve productivity, drive operating efficiencies and transform the way many types of products are mass-produced. Benefits include optimized efficiency and reduced assembly line errors.

Those trends are forcing manufacturers in many industries to invest in new tools and technologies, such as additive manufacturing, collaborative robots, data analytics and wearable devices.

The 22nd annual ASSEMBLY State of the Profession survey finds that almost one-half (49 percent) of respondents will be allocating more resources toward assembly operations during the next 12 months. That’s 7 percentage points higher than in 2016.

Specifically, use of collaborative robots is up 5 percentage points, while deployment of wearable devices is up 2 percentage points. And, almost two-thirds (61 percent) of respondents believe that new digital tools and smart technology will help them improve productivity, while 60 percent say it will lower production costs.

Additive manufacturing is also transforming the way products are designed and made. More than one-third (44 percent) of State of the Profession respondents plan to use 3D printing technology during the next 12 months. That’s a 7 percentage point increase over 2016 and 13 percentage points higher than 2015.

“We are now in the digital industrial revolution,” says Jean-Pierre Petit, global head of digital manufacturing at Capgemini, a global consulting company that recently conducted a survey on the topic through its Digital Transformation Institute. “The impact on overall efficiency will be profound. The next few years will be critical as manufacturers step up their digital capabilities and accelerate their digital outcomes to maximize company benefits.

“As a result of productivity, efficiency and flexibility improvements, smart factories will benefit from significant reductions in operating costs,” claims Petit. “For example, the average automotive manufacturer could drive up to a 36 percent improvement in operating margin through improved logistics and material costs, equipment effectiveness and improved production quality.”

Looking for quick answers on assembly and manufacturing topics? Try Ask ASM, our new smart AI search tool. Ask ASM

One company that’s ahead of the curve is Faurecia, a $23 billion Tier 1 supplier that operates more than 100 facilities around the world. It recently opened a new emission control systems assembly plant in Columbus, IN, that features state-of-the-art production equipment and processes that capitalize on smart devices, embedded intelligence and data analytics.

“We are seeing [great] success in our employees working alongside intelligent tech,” says Gregoire Ferre, chief digital officer at Faurecia. “Launching greenfield smart factories, as well as digitizing [existing] plants, are key building blocks of our digital transformation program. We are also seeing success in revamping old processes to be more efficient and using technology as part of our predictive maintenance scheme, all of which save our employees time.”

Another manufacturer that’s harnessing technology to gain a competitive advantage is General Electric.

“New technologies and business models have…manufacturing on the verge of an innovative new period that promises greater productivity and the potential for lower costs,” claims Andy Henderson, Ph.D., industry analyst for discrete manufacturing at GE Digital. “[There’s a] concerted effort to move manufacturing to its smarter, more efficient, more innovative future.

“Supply chain models are adding efficiencies, and smart sensors and automation technologies are making factories more efficient and safer than ever before,” adds Henderson. “Emerging technologies and digital transformation will allow players to jockey for competitive advantage through innovation in time-to-market, speed of innovation, improvement in process and reduction of costs.”

According to Henderson, data-driven manufacturing is one of the today’s hottest trends. “Cheap and ubiquitous sensing has afforded an unprecedented ability to gather huge amounts of granular process data in real-time,” he points out. “These sensors, along with the data they generate and the analytic tools to process that data, make up the connected network of the Industrial Internet of Things, and are critical elements of the next-generation factory.”

Indeed, more than one-fourth (29 percent) of assemblers responding to ASSEMBLY’s 2017 State of the Profession survey claim their company will be investing in data analytics this year.

However, large manufacturers (companies with 2,000 or more employees) are more likely to invest in data analytics (70 percent) vs. only 24 percent of small manufacturers (companies with 100 or fewer employees).

Data analytics is more popular with assemblers in the medical equipment (57 percent), aerospace (34 percent) and transportation equipment (29 percent) industries.

Localization

Another trend that’s transforming the manufacturing landscape is protectionism and localization.

“The rise of protectionism is changing how global companies think about expanding, and where they might locate their facilities,” says Henderson. “If the transition to a more localized economy is more than temporary, we can expect to see more companies emphasizing local production and distribution of heavy manufacturing output.”

“Localization—production in the market where the product will be consumed—is a strategy increasingly used by many large companies to shorten supply chains and reduce shipping costs,” adds Harry Moser, founder and president of the Reshoring Initiative. “Offshoring has slowed considerably.

“Avoiding globalization for its own sake brings economic strength and stability,” claims Moser. “Localization also yields a green benefit. It reduces world environmental impacts through reduced carbon emissions from producing in developed countries and from much shorter transport.

“We have gone from globalization at any cost to our economy, long-term company sustainability and the world environment to recognizing that via localization, a company often can embrace all of these benefits while maintaining or improving profitability,” Moser points out.

The localization trend should result in the construction of new domestic assembly lines.

In fact, almost one-third (29 percent) of State of the Profession respondents work for companies that plan to expand existing facilities or build new plants during the next 12 months. That’s 6 percentage points higher than in 2016.

Construction activity will be strongest in the fabricated metals (35 percent), contract manufacturing (34 percent), electrical equipment and appliances (34 percent) and transportation equipment (29 percent) industries.

Large manufacturers (companies with 2,000 or more employees) plan to build the most infrastructure (58 percent vs. 30 percent of small manufacturers). More than one-third (40 percent) of respondents in the South anticipate plant expansions during the next 12 months, followed by the West (32 percent), Midwest (27 percent) and Northeast (16 percent).

With all that positive news, overall job satisfaction levels are at a record high. More than one-half (54 percent) of assemblers claim they are “highly satisfied,” which is 2 percentage points higher than 2016.

The bullish outlook of the 2017 State of the Profession report is mirrored in studies conducted by other organizations. For instance, more and more manufacturers are discovering that it’s often more profitable to produce or source domestically.

In fact, for the first time in decades, more manufacturing jobs are returning to the United States than are going offshore. According to the Reshoring Initiative, new U.S. manufacturing jobs attributed to reshoring and foreign direct investment (FDI) totaled 77,000 in 2016. That’s a 10 percent increase over 2015, exceeding the rate of offshoring by about 27,000 jobs.

This trend contrasts the period from 2000 to 2003, when the United States lost approximately 220,000 manufacturing jobs per year to offshoring.

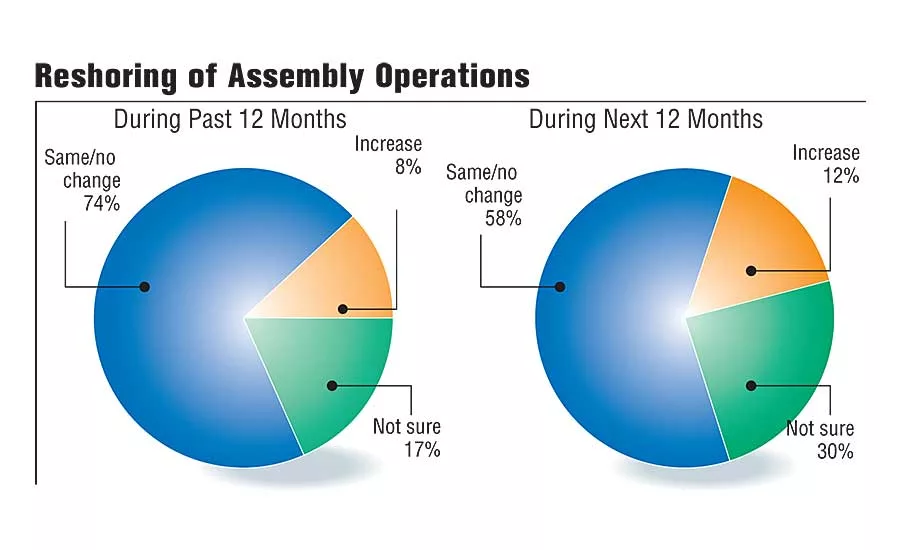

Eight percent of State of the Profession survey respondents claim that their company reshored assembly operations during the last year. And, 12 percent expect their companies to bring work back to the states during the next 12 months.

Large manufacturers (companies with 2,000 or more employees) are more likely to reshore. More than one-quarter (27 percent) of respondents in that category plan to shift assembly operations back to the United States during the next 12 months vs. 16 percent of small manufacturers (companies with 100 employees or less).

One-third (33 percent) of ASSEMBLY respondents in the plastics and rubber products industry expect their company to reshore operations during the next 12 months. The computer and electronics (21 percent) and transportation equipment (20 percent) sectors also will see more reshoring activity in the near future.

“The tide has turned,” claims Moser. “The numbers demonstrate that reshoring and FDI are important contributing factors to the country’s rebounding manufacturing sector.

“The overall trend was up from 2015, due to anticipation of potential policy changes that will make the United States more competitive, continued rising wages overseas, and increased use of total cost of ownership for sourcing decisions,” explains Moser.

“Proximity to customers was the leading factor for reshoring, followed by government incentives, skilled workforce availability and ecosystem synergies,” adds Moser. “The Southeast and Texas remain the top regions for reshoring and FDI, with the Midwest in second place due to its strong industrial base.”

ASSEMBLY’s study confirms this trend. Indeed, 13 percent of respondents in the Midwest expect their company to reshore manufacturing during the next 12 months vs. 11 percent in the South.

“There are still huge opportunities and challenges to bringing back all the 3 million to 4 million manufacturing jobs cumulatively lost to offshoring,” warns Moser. “However, preliminary 2017 data trends are looking to be at least as good as 2016.”

Economic Headwinds

Manufacturers are buckling their seat belts to ride the economic rollercoaster ahead. That’s because the MAPI Foundation, the research affiliate of the Manufacturers Alliance for Productivity and Innovation, is forecasting modest U.S. economic performance for the next 12 months. It predicts manufacturing production growth of only 1.2 percent in 2017, increasing to 2.6 percent in 2018.

“The harsh reality of historically slow global economic performance remains in place, and the U.S. economy and U.S. manufacturing sector continue to confront a host of performance-impeding challenges,” warns Cliff Waldman, chief economist at the MAPI Foundation. “Capital spending, a key demand driver for the U.S. factory sector, is still far weaker than the low double-digit growth rate that was once the norm for equipment investment growth.

“This longstanding problem has created an almost structural demand deficit for U.S. manufacturers,” explains Waldman. “Further, weak capital spending is one factor in a sluggish productivity picture for the economy and manufacturing, with a host of implications for future growth, wages and living standards.

“While world growth might be slightly firming and strengthening, the global bias toward the dollar is unlikely to change in the next few years,” adds Waldman. “The meaningful gaps in economic growth and interest rates between the U.S. and the rest of the world are likely to remain favorable to the greenback. This is a frustrating, profit-killing problem for U.S. manufacturers that struggle for price advantage in a difficult global business environment.

“Normal forecast uncertainty is growing, as political and policy uncertainty are rapidly rising as elements of the U.S. manufacturing growth outlook,” says Waldman. “The potential flow of new U.S. tax, regulatory, healthcare and trade policies could very well add a measure of dynamism and rapid change for the short-term manufacturing growth outlook, the likes of which have not been seen in quite some time.”

ASSEMBLY’s 2017 State of the Profession study was conducted in March, amidst relatively positive economic news. It was just a few weeks after President Trump told chief executives of major U.S. companies that he plans to bring millions of manufacturing jobs back to the United States through new tax and regulatory policies.

According to the U.S. Bureau of Labor Statistics, the unemployment rate hovered at 4.5 percent in March. At the same time, 12.4 million Americans worked in manufacturing. That was up by about 25,000 jobs from a year prior, and almost a million from early 2010.

Meanwhile, the National Association of Home Builders (NAHB) claimed that sales of newly built, single-family homes rose for the third straight month, increasing 5.8 percent in March. Those sales numbers were the second highest on record since the Great Recession.

“Fueled by a growing economy, solid employment gains and rising household formations, single-family production will continue on a gradual, upward trajectory in 2017,” says Robert Dietz, NAHB chief economist. “While positive developments on the demand side will support solid growth in the single-family housing sector in 2017, builders in many markets continue to face supply-side constraints led by the three Ls— lots, labor and lending.”

However, Dietz says builder confidence is up in anticipation that the Trump administration will help lower regulatory costs. “Regulatory requirements make up nearly 25 percent of the cost of a new home,” he points out. “Given those constraints, it is hard to build a $200,000 entry-level house.”

Another positive economic indicator in March was AMT’s U.S. Manufacturing Technology report. Orders for new production equipment were up 35 compared to the previous month, and up more than 3 percent over March 2016.

“An increase for the month was expected, since it marked the end of the fiscal year for many companies, but it’s encouraging to see the last two months outpacing their 2016 levels—the possible start of an upward market trend,” says Douglas Woods, AMT president. “When manufacturers make investments to boost their capacity and productivity, it’s a good sign for a strengthening manufacturing economy.

“Leading indicators show that promising gains for manufacturing are likely to continue,” adds Woods. “Consumer sentiment is on the rise, which will lead to more purchases of durable goods like cars, appliances, electronics and housing.”

The National Association of Manufacturers (NAM) claims that March was the third straight month of manufacturing job growth. Although the Trump administration has been controversial, NAM believes it’s benefitting all types of U.S. manufacturers—partially because U.S. manufacturers are burdened by more than 297,000 regulatory restrictions.

“Across America, manufacturers’ optimism is soaring, in no small part because of President Trump’s laser-like focus on pursuing bold action, particularly on rethinking red tape to address regulatory reform, to accelerate a jobs surge in America,” claims Jay Timmons, NAM president and CEO. “Manufacturers of all sizes are now less concerned about the business climate going forward because they are counting on President Trump to deliver results.

“Small manufacturers—more than 90 percent of our membership—are among the hardest hit by regulatory obstacles,” adds Timmons. “Costs for small manufacturers with fewer than 50 employees total almost $35,000 per employee per year—money that could otherwise go to creating jobs. It’s encouraging to see an administration so focused on providing regulatory relief to spur manufacturing growth.”

According to NAM, manufacturers’ economic optimism is at a record 20-year high.

“President Trump’s actions have certainly boosted manufacturers’ confidence in the future, and that positive change is coming,” explains Timmons. “The president is rethinking red tape and addressing our regulatory burden, helping us to create American jobs and grow our economy.

“But, we are still far from reaching our full potential,” warns Timmons. “An outdated tax code, crumbling infrastructure and excessive regulations make it unnecessarily difficult to compete and win against overseas competitors.”

The optimism coming out of Washington is reflected in ASSEMBLY’s 2017 survey. A majority (93 percent) of respondents expect their company to commit either the same amount or more resources toward operations during the next 12 months. That’s 3 percentage points higher than in 2016.

Manufacturers in the transportation sector, which includes automobiles, car parts, motorcycles, recreational vehicles and trucks, are the most optimistic. Indeed, 49 percent of those assemblers claim their companies will be committing more resources toward improving operations.

Auto Industry Stays Hot

After several years of record sales, the U.S. auto industry is expected to experience a slight decline in 2017. The 17.4 million vehicles sold in 2016 will drop to 17.1 million this year. But, there’s no shortage of optimism in the industry.

“The strong economic growth that propelled new-vehicle sales to back-to-back record years in 2015 and 2016 is on pace to continue in 2017,” claims Steven Szakaly, chief economist at the National Automobile Dealers Association (NADA). He points to a number of factors, including positive GDP growth, an excellent employment rate, rising consumer confidence, positive equity markets and stable oil prices.

“Our baseline forecast…is a slight decline of about 350,000 units [from 2016], but it is still a very, very strong year,” notes Szakaly. “Fundamentally, I think consumers are at a point where the market, while not saturated, is now reaching a plateau, and that is why we are looking at sales declining.”

Szakaly also believes there’s an alternative scenario that could see sales in 2017 and 2018 eclipse even last year’s record. “A lot has changed, particularly in Washington,” he points out. “Let’s say that President Trump passes all of his tax cuts and all of his infrastructure spending. That is going to be a big boost to economic growth and economic activity. If that happens, we could easily see another year or two of [record] new-vehicle sales.”

While he admits there are some economic headwinds on the horizon, Szakaly says “overall, we still expect sales and leases to reach 17.1 million new vehicles in 2017, with the expectation that rising consumer incentives will overcome any increases in interest rates later in the year. While these headwinds will not have much of an impact on new-vehicle sales, they are a sign of a flat market as we look [ahead to] next year.”

According to Szakaly, consumer demand for new vehicles remains strong. But, he sees a mixed bag of positives and negatives shaping the new-vehicle market ahead.

“One area that does not get nearly enough attention in the consumer demand equation [for new vehicles] is technology and safety, particularly the combination of the two in the form of advanced driver assistance systems,” says Szakaly. “Across the fleet, there is strong demand for vehicles equipped with the latest safety features, such as automatic emergency braking, lane-departure warning systems and collision avoidance technology. This is a big piece of the overall new-vehicle demand puzzle.”

On the flip side, factors that could adversely impact new-vehicle sales include longer auto loan terms and higher interest rates that stretch out the buying cycle. In addition, Szakaly says a large supply of off-lease used vehicles entering the market will likely pull some new-car buyers into the used-vehicle market.

Globally, 2017 light vehicle sales should reach 93.5 million units, a growth rate of 1.5 percent over 2016.

“However, industry risk in mature markets is at the highest level it has been since…the global downturn from 2008 to 2010, and will be a key factor for the near future,” warns Henner Lehne, senior director of the global vehicle group at IHS Markit, a market analysis firm that specializes in the auto industry. “Engine propulsion options are expected to have an influence as well.

“It is difficult (and unlikely) to sustain and continue to grow at the same rates the U.S. market has seen over the past eight years, and a leveling off is underway,” claims Lehne.

“Political uncertainty could cause a significant rift in light vehicle sales both in the U.S. and Europe, as both regions are undergoing fluctuations in policy, leadership and other dynamics,” adds Lehne. “The policies and changes proposed by the Trump administration regarding trade and environmental regulations create some uncertainty, countered by a slightly improved economic picture for 2018 to 2021.”

Over the next three years, automakers plan to ramp up the speed at which they replace models. In fact, the number of vehicle launches will average more than 50 a year from 2017 to 2020.

That’s why OEMs and suppliers are currently pouring billions of dollars into their domestic assembly plants. According to the State of the Profession study, 29 percent of assemblers in the transportation sector work for companies that are expanding current facilities or building new plants.

Toyota plans to invest $10 billion in the United States over the next five years, including a $1 billion dollar investment at its flagship assembly plant in Georgetown, KY. Meanwhile, Honda intends to pump $85 million into its Lincoln, AL, plant.

The Detroit 3 is also getting in on the spending spree. General Motors plans to invest $1 billion in its domestic operations. Ford Motor Co. is putting more than $1 billion into three Michigan facilities to prepare for production of the all-new Bronco SUV and Ranger pickup, and to support the company’s expansion into mobility.

Fiat Chrysler is spending $1 billion to overhaul its assembly plants in Michigan and Ohio to build the upcoming Jeep Wagoneer, Grand Wagoneer and Wrangler pickup. The move will add 2,000 jobs to the automaker’s U.S. workforce and will enable the company to move Ram heavy-duty pickup truck production from Mexico to the U.S.

Tier 1 suppliers are also investing heavily in new facilities to boost productivity, improve throughput and address quality concerns.

For instance, Continental Automotive Systems is spending $40 million to expand its brake assembly plant in Morganton, NC. Faurecia Clean Mobility, a global manufacturer of automotive emission control systems, is building a new $4 million assembly plant in Fort Wayne, IN.

Salaries Remain Stable

The typical State of the Profession respondent is 54 years old, has 24 years of experience and earns $97,217. However, there are exceptions at both the high and low ends of the scale. For instance, 36 percent of respondents take home less than $75,000 per year, while 35 percent earn more than $100,000.

On average, men earn 21 percent more than women. And, more than one-quarter (26 percent) of women respondents earn less than $60,000 vs. 18 percent of men. Part of this discrepancy is due to the fact that women make up almost 50 percent of the U.S. labor force, but only about one-quarter of the country’s manufacturing workforce.

Many female respondents to ASSEMBLY’s survey also have less experience than their male counterparts. Women represented only 5 percent of respondents and had an average of 17 years of experience vs. 24 years for men.

In fact, more than three-quarters (78 percent) of men have more than 15 years of experience in the assembly field, while 33 percent of women have less than 15 years of experience.

In addition to gender, several other factors determine pay rates, such as age, education, experience, location and type of industry.

Industry experience is the biggest factor that determines compensation. Individuals with more than 25 years of experience (46 percent of respondents) typically earn more than assemblers with less than 15 years of experience in the assembly field (30 percent of respondents).

Assembly professionals tend to be loyal employees who stay with the same company for many years. In fact, 40 percent of respondents have worked at the same firm for more than 10 years, while 15 percent have been with their present employer for less than three years.

More than one-half (61 percent) of ASSEMBLY’s respondents received a pay increase over the last 12 months. Only 4 percent experienced a decrease in salary. Salary raises varied widely, but the average increase was 7 percent, which is 2 percentage points higher than in 2016 and 3 percentage points higher than in 2015.

Almost one-half (49 percent) of respondents received a cash bonus during the last 12 months. Bonuses were typically tied to factors such as overall company and plant performance, in addition to implementing successful cost reduction programs, meeting deadlines for new projects and launching new products.

More than one-half (61 percent) of assemblers who work in the fabricated metals and medical equipment industries received a cash bonus during the past year, followed by assemblers in the machinery (56 percent), computer and electronics (51 percent) and contract manufacturing (49 percent) sectors.

Almost two-thirds (65 percent) of assembly professionals expect to receive a salary increase at their next review. Assemblers in the computer and electronics industry feel most confident about receiving a raise in the near future.

Indeed, 84 percent of those individuals say they expect a raise, followed closely by assembly professionals in the transportation equipment (76 percent), fabricated metals (74 percent), contract manufacturing (72 percent) and aerospace (68 percent) industries.

However, respondents who work for plastics and rubber manufacturers are less optimistic. Only 34 percent of them expect to receive an increase in their salary during the next 12 months.

More than one-half (63 percent) of assemblers at large companies (manufacturers with 1,000 or more employees) received a cash bonus during the past 12 months vs. only 42 percent of assemblers at small manufacturers. Assembly professionals who work for larger manufacturers are also more likely to receive a raise during the next 12 months.

However, assemblers who work for smaller firms tend to be much happier (61 percent) than people who work for big companies (48 percent).

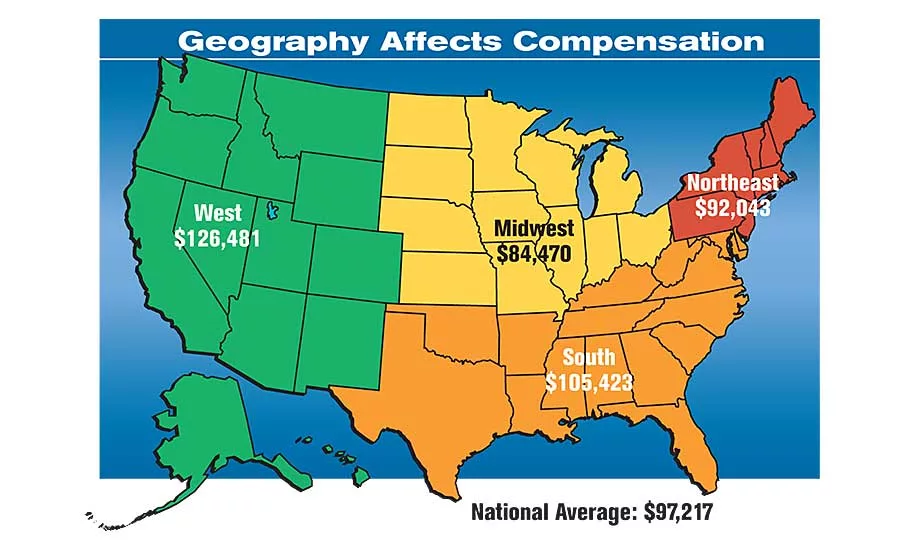

Geography Lesson

Assembly salaries typically fluctuate from region to region, due to the local cost of living. For instance, while you’d need to make upwards of $100,000 to afford a home in San Francisco, that number drops to around $20,000 for one in Pittsburgh.

The West (Arizona, California, Colorado, Idaho, Montana, Nevada, New Mexico, Oregon, Utah, Washington and Wyoming), which is home to 16 percent of State of the Profession respondents, boasts the highest salaries—an average of $126,481.

On the other hand, assemblers in the Midwest (Illinois, Indiana, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, Ohio, South Dakota and Wisconsin), which is home to 39 percent of respondents, average $84,470.

Assembly professionals in the South (Alabama, Arkansas, Delaware, Florida, Georgia, Kentucky, Louisiana, Maryland, Mississippi, North Carolina, Oklahoma, South Carolina, Tennessee, Texas, Virginia and West Virginia), which is home to 26 percent of respondents, average $105,423.

With an average salary of $92,043, the Northeast most closely resembles the national average of $97,217. That region is home to Connecticut, Maine, Maryland, Massachusetts, New Hampshire, New Jersey, New York, Pennsylvania, Rhode Island and Vermont.

Only 30 percent of assembly professionals in the South earn more than $100,000 vs. 54 percent of assemblers in the West.

Assemblers in the Northeast tend to work two hours a week more than the national average of 46 hours, while assemblers in the West work two hours less. However, 28 percent of respondents in the West expect to work more hours during the next 12 months vs. 18 percent of assemblers in the Northeast.

Assembly professionals in the Northeast tend to be more satisfied than their peers in other parts of the country. More than three-fourths (77 percent) claim to be “extremely satisfied” vs. 41 percent of assemblers in the South.

The size of a manufacturer typically determines compensation levels. For instance, assemblers who work at companies with more than 2,000 employees earn an average of $99,233 Assembly professionals at companies with less than 50 employees earn an average of $86,373.

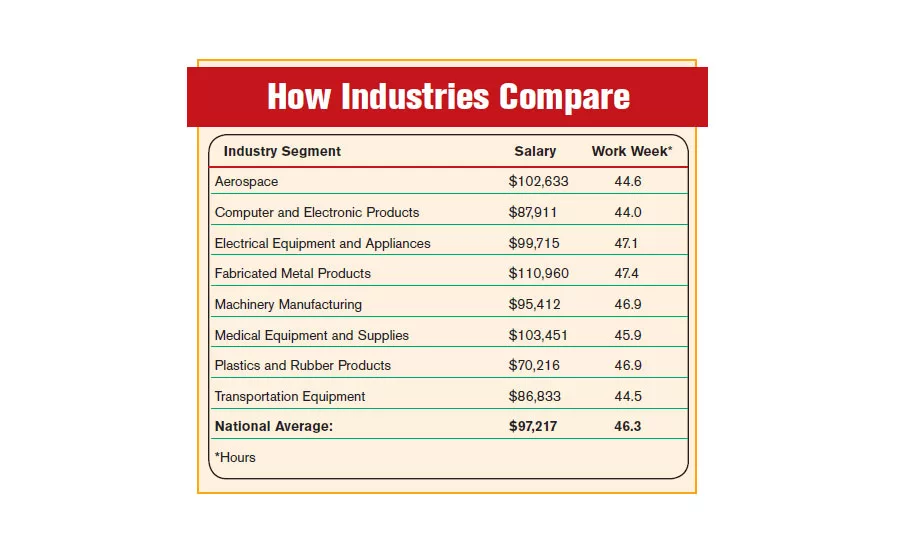

Assemblers in the fabricated metal products sector receive higher salaries than their peers in other industries. For instance, they earn 12 percent more than the national average of $97,217. Assembly professionals in the aerospace, electrical equipment and appliances, and medical equipment industries also receive higher-than-average compensation.

However, assemblers in the fabricated metal products industry also work longer weeks than their peers elsewhere.

Manufacturing engineers (23 percent of respondents) earn slightly more than design engineers (7 percent of respondents). According to the 2017 State of the Profession survey, manufacturing engineers earn an average of $84,227 vs. $82,451 for design engineers.

Salaries also fluctuate widely based on type and level of education. For example, assembly professionals with just a bachelor’s degree (40 percent of respondents) earn an average of $102,095. However, assemblers who’ve earned a master’s degree (17 percent of respondents) earn $110,224.

Obtaining a master’s in business administration (MBA) or a professional certification, such as a P.E., is a good way to ensure a higher salary. Assemblers with MBAs (10 percent of respondents) earn an average of 21 percent more than non-MBAs. Assembly professionals who are P.E.s (6 percent of respondents) earn an average of 12 percent more than others.

Age is another critical factor that affects compensation. For instance, assembly professionals who are more than 50 years old (69 percent of respondents) typically earn the highest salaries. They average $111,577 vs. assemblers who are under 40 (14 percent of respondents), who earn an average of $70,938.

The percentage of older employees is growing. Indeed, 34 percent of 2017 State of the Profession respondents are 60 years old or older. That’s 5 percentage points higher than in 2016 and 10 percentage points higher than 2015.

That trend is expected to continue for a few more years. According to the Employee Benefit Research Institute, 19 percent of Americans aged 65 and older are still working. That’s the highest rate since the early 1960s. And, almost one-third of workers in that age group say they expect to work until at least 70.

No Time to Rest

Lack of time is perceived to be the No. 1 on-the-job constraint that assemblers face today. More than one-half (58 percent) of 2017 State of the Profession respondents complain about time constraints. That’s 2 percentage points higher than in 2016.

Time-related pressure will pose the biggest challenge to assemblers who work in the medical equipment (77 percent), aerospace (66 percent), machinery (63 percent) and transportation equipment (58 percent) industry.

Assembly professionals at manufacturers with 2,000 or more employees are under more pressure to watch the clock than people who work for manufacturers with less than 50 employees. Indeed, more than two-thirds (72 percent) of respondents at large companies cite time constraints as a challenge vs. only 48 percent of assemblers who work at small firms.

And, 20 percent of assembly professionals believe their average work week will increase during the next 12 months, which is 2 percentage points higher than in 2016 and 6 percentage points higher than in 2015.

More than one-quarter (28 percent) of assembly professionals who work in the medical equipment industry expect to work more hours during the next 12 months, followed by assemblers in the aerospace (25 percent) and computer and electronics (22 percent) industry.

Assemblers at large manufacturers plan to spend more time at work than their counterparts at smaller companies. Only 19 percent of respondents who work for manufacturers with less than 100 employees expect to work more in the next 12 months. However, 29 percent of assemblers who work for companies with more than 1,000 employees will experience longer work weeks.

Assembly professionals work an average of 46 hours a week. In fact, almost two-thirds (65 percent) of 2017 State of the Profession respondents often work more than 45 hours a week. People in the fabricated metal products typically spend the most time at work (an average of 47 hours per week), while assembly professionals in the computer and electronic products industry work less (an average of 44 hours per week).

The majority (64 percent) of participants in ASSEMBLY’s study say that they are doing the same amount of work-related travel today vs. one year ago. Eighteen percent of assemblers claim they are doing more travel.

In addition to time management, assembly professionals will spend more time dealing with the skilled labor shortage. More than one-third (42 percent) of 2017 State of the Profession respondents claim they are struggling to staff their assembly lines. That’s 4 percentage points higher than in 2016.

Both large and small manufacturers claim they are having trouble finding skilled workers. More than one-third (44 percent) of companies with 100 or fewer employees and 48 percent of companies 1,000 or more employees face that challenge.

Almost two-thirds (65 percent) of respondents in the plastics and rubber products industry will be focusing on finding employees during the next 12 months. Other industries affected by the skills gap include contract manufacturing (62 percent), fabricated metal products

(55 percent), electrical equipment and appliances (54 percent), computer and electronic products (49 percent) and transportation equipment (42 percent).

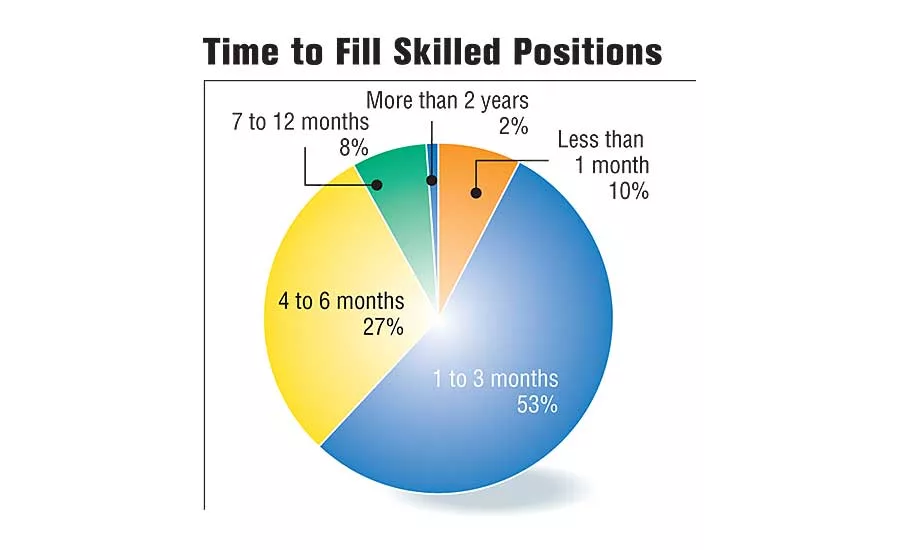

More than one-half (53 percent) of assemblers claim that it now takes an average of one to three months to fill openings on their production lines. That’s 7 percentage points higher than in 2016.

Technology Trends

Another big constraint facing assembly professionals today is finding ways to implement technology to boost productivity, improve quality and reduce time to market. More than one-third (41 percent) of State of the Profession respondents claim that they’re spending more time trying to make new technology work.

One of the biggest trends today is human-machine collaboration. Next-generation machines equipped with state-of-the-art sensor technology allow robots to operate side-by-side with humans. Because they are flexible and require little or no safety barriers, collaborative robots are being used by a wide variety of manufacturers, including Continental Automotive Systems and Whirlpool Corp.

Almost one-third (31 percent) of assemblers plan to deploy collaborative robots during the next 12 months. The machines particularly appeal to large manufacturers. Indeed, more than three-quarters (80 percent) of companies that employ 2,000 or more people are interested in the technology vs. only 13 percent of companies with 50 or fewer employees.

More than one-third (44 percent) of manufacturers in the transportation equipment sector plan to invest in collaborative robots. Other industries eager to allow humans and robots to work in close proximity on assembly lines include machinery (39 percent), plastics and rubber (39 percent), medical equipment (38 percent), aerospace (33 percent) and contract manufacturers (29 percent).

Wearable devices are another technology that’s becoming more popular in manufacturing today. Devices such as glasses, smartphones and tablets enable assemblers to easily access important information, such as work instructions.

Nine percent of State of the Profession respondents plan to deploy such technology on the plant floor in the next 12 months. Large manufacturers (18 percent) are more likely to deploy wearable technology vs. only 3 percent of small manufacturers.

Smartphones are popular with more than one-half (60 percent) of assemblers. Other wearable technology being deployed on assembly lines include tablets (59 percent), glasses (38 percent), gloves (37 percent) and watches (12 percent).

Aerospace manufacturers (11 percent) plan to use the most wearable devices, followed by the medical equipment (10 percent) and transportation equipment (9 percent) sectors.

Survey Methodology

ASSEMBLY magazine would like to thank all the respondents who participated in its 22nd annual State of the Profession survey. The survey was conducted online in March 2017 by BNP Media’s market research division. It was sent to more than 29,000 randomly selected subscribers with an e-mail address.

The charts and tables in this report highlight the major data gleaned from the survey responses. On some of the questions, the response rate does not equal 100 percent due to rounding or surveys that contained one or more unanswered questions. In cases where multiple responses were allowed, the total may exceed 100 percent.

Special thanks to Jessica Langer for her assistance with online survey design, distribution and tabulation.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!