Product Design: Design First, Lean Second

DFMA enables engineers to design products that are lean from the start.

Lean manufacturing has revolutionized how companies bring their products to market. But, while engineers have excelled at eliminating waste in the assembly process, they don’t always take an equally vigorous approach to the product itself. Designing a product for efficient manufacture and assembly can eliminate waste before the product even reaches the line.

It has long been established that 70 percent of a product’s cost is determined at the design phase. Once the product is being manufactured, engineers have few options to reduce costs without starting over.

Once production has begun, major design changes can incur not only large costs but also significant risk. Without an analysis of the design for manufacture and assembly (DFMA), production managers have difficulty knowing the financial impact of late-stage design fixes. And since there is an assembly already in production for which most costs are known, it’s much easier to look exclusively for savings through lean manufacturing.

In the long-term, however, this approach is problematic. Lean manufacturing, kaizen and Six Sigma are valuable techniques, but they do not address the causal relationship between part design and production efficiency.

Manufacturers also need a way to understand the cost trade-offs associated with changes in the product design, the manufacturing process, and the materials used to make each part. When this information is in the hands of engineers early in the design phase, they can make better decisions about costs. This is what a DFMA analysis provides.

DFMA is comprised of two parts. Design for assembly (DFA) is a quantifiable methodology for consolidating parts and simplifying the product. Design for manufacture (DFM) is a systematic approach to reducing costs by examining manufacturing processes and material choices.

A DFMA analysis early in the design stage can yield more savings than can lean manufacturing once the design is set and production is underway.

Designing for function alone consumes large blocks of time in the development process, creating the perception that there is no time for anything else. However, studies have shown that an increase in time spent during the concept phases of product development-including a DFMA analysis-can actually shorten time to market.

An additional benefit of a DFMA analysis is that the design team understands costs before assembly begins, enabling them to make decisions that can influence the final cost of the product. In a more traditional development cycle, it’s less likely that they will be able to make changes later on.

For example, if a team designs a part to be produced by flame-cutting carbon steel and machining it to final shape, they will have few alternatives if they later discover that costs are too high. Tooling may have already been purchased, the supply chain established, and parts may even be rolling off the line.

In that situation, lean manufacturing looks like a good idea. With lean, the product design won’t change, so there is little risk in undertaking the effort. And simple changes in the process can have some benefit. Engineers can reduce setup and changeover time, switch to a more efficient supplier, or change sheet size and material usage.

But, if the design is scrutinized early in the development cycle, the engineering team might realize that forging the part to a near-net shape is much more cost-effective than cutting and machining it. Comparing the two processes is a fairly simple exercise during design, yet knowing which process makes the most sense financially is something most design teams struggle with.

It is important not only to understand the cost of a design, but the distribution of that cost as well. When design teams document this, they can focus their efforts to gain the greatest impact. Given that 75 percent of the cost of the part is in the material, looking for savings through improved setup is a relatively fruitless exercise. Setup consumes a small portion of the total cost.

While these principles hold true for components, the same ideas apply to whole products. About 70 percent of the total cost of most products is tied up in parts. The other 30 percent is labor and overhead.

Given this cost breakdown, it becomes obvious that a focus on the piece-part cost will have the most impact on the overall cost of the product. So while a discussion about manufacturing processes and material combinations for individual parts is essential, engineers should concentrate on simplifying their designs.

Product simplification can be defined as the challenge to come up with a design that meets the required functionality with the fewest parts. It can be accomplished using a classic DFA analysis. When applied at the early stages of design, DFA can have far-reaching impacts on cost.

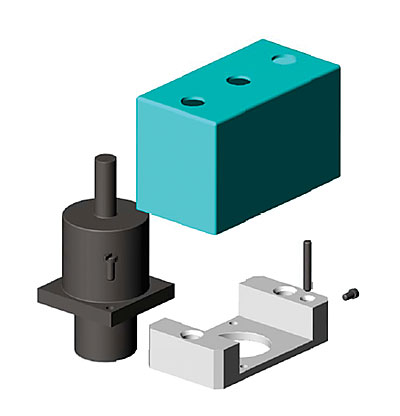

Applying lean manufacturing to a product like the motor assembly in Fig. 1 could certainly have some effect on its cost. Fig. 2 shows how DFM and DFA analyses can simplify the product. Assuming both designs meet performance requirements, you can see how changes to the original design can have a bigger impact on cost than anything that could be achieved through lean manufacturing.

Comparing the two designs, the redesigned assembly has 12 fewer parts. That results in 12 fewer drawings and digital models to maintain, 12 fewer suppliers to qualify, 12 fewer service parts to consider, 12 fewer items to inventory, and so on. The redesign also costs 46 percent less.

In short, efforts to cut costs using lean have focused on the wrong area. To achieve the most impact, our efforts need to be pushed upstream to the design stage.

When they understand the costs on a product’s bill of materials, the design team can influence those numbers in three ways.

First, they can provide the supply chain group with the results of their cost modeling. This information is invaluable when negotiating with suppliers. No longer will the purchasing department need to send drawings to suppliers, wait weeks for quotes, try to make sense of the numbers, and finally select a supplier. Instead, prior to the quoting process, they will already know what the parts should cost. They can then use this information to make better buying decisions.

Second, if modeling indicates that product costs do not meet projected profit margins, the design team can use DFM techniques to investigate trade-offs at the piece-part level. Choices of manufacturing processes and material combinations, along with minor changes in the design of the individual parts, can have an impact on cost. Through early analysis, these outlays can be documented, and data-driven decisions can be made.

For example, let’s say a design called for a sand-casted metal part purchased through a domestic source at a cost of $4.81 per part. Then, to save money, the company opts to outsource the component to a low-cost region. Cost-modeling techniques allow us to challenge the choice of manufacturing process as well as the design of the component itself.

Through cost-modeling, we can see that die casting the part through a domestic source ($3.50 per part) is actually less expensive than sourcing a sand casting from a low-cost region ($3.82 per part). The next logical question is whether outsourcing the die casting would make even more sense. At first pass, it does, since a low-cost region can supply the part at $3.35 per piece.

However, these prices are just the cost to manufacture the part. Other costs need to be taken into account to make an apples-to-apples comparison between all the alternatives. Once logistics, shipping, communications and other costs are considered, it’s likely that sourcing the die casting from the low-cost region could not be justified. In the end, die casting the part through a domestic source makes the most economic sense.

The third way a design team can influence the costs on a bill of materials is to review the design of the product itself. The most effective way to reduce costs is to reduce the number of parts required for the product to accomplish its desired function. In addition to generating labor time estimates, a DFA analysis helps the design team determine a theoretical minimum part count.

To accomplish this, three questions are asked of each part to justify its being separate, by necessity, from all other parts in the product:

DFA Index = (NM x 2.93)/TA.

In this equation, NM represents theoretical minimum number of parts, and TA stands for total operation time.

This index represents the efficiency of the design from an assembly perspective. It helps guide the team by comparing the part count in an existing design with what is possible to achieve. Generally, the higher the DFA Index, the better the design from a cost perspective.

DFA leads to dramatic savings and a more efficient manufacturing process that will ultimately result in more significant savings than could be achieved with lean manufacturing alone.

For example, consider the four designs in Fig. 3. The one on the far left is complex. Once in production, it will be difficult to produce cost-effectively. However, the three designs on the right have been progressively designed using DFA to be less expensive and easier to make. Once the design on the left is in production, no additional efforts can realistically come close to producing a product with a cost as low as one designed right the first time.

To see how this might work, let’s cost out a steel spacer plate. The square part is 4 inches wide, 4 inches tall, and 0.188 inch thick. It has a 1.75-inch diameter hole in the center and one 0.375-inch diameter hole in each corner. After a 1/4-20 self-clinching fastener is pressed into each corner hole, the assembly is powder-coated with a black finish.

Using established cost models, we can determine what the assembly should cost.

Weight. Let’s assume that this part will be laser-cut from a sheet of carbon steel and produced in an annual volume of 1,000 parts. Geometry and the density of the steel tell us that the blank weighs 0.851 pound. The material cut from the part weighs 0.151 pound, resulting in a part weight of 0.7 pound.

Cost of a sheet. Let’s assume this part will be cut from a 36- by 36-inch sheet. Allowing for 0.375 inch of clearance from part to part and from part to edge, we will get eight parts along the width of the sheet and eight parts along its length, or 64 parts in total.

We can calculate the weight of the sheet at 68.952 pounds. Assuming a cost of $0.41 per pound for the steel and a value of $0.04 per pound for the scrap left over from the sheet and for the holes cut from the part, we can calculate the cost of a sheet as $28.27.

Scrap value. The scrap from the sheet is the weight of the sheet less the weight of the 64 blanks cut from it: 68.952 pounds - (64 x 0.851 pound) = 14.488 pounds. The scrap from the holes is weight of the holes times the number of parts: 0.151 pound x 64 = 9.664 pounds. Thus, the total scrap produced from one sheet is 24.152 pounds. Given the scrap value of the material, we can calculate a scrap value of $0.966 from the sheet.

Material cost per part. The material cost per part is the cost of the sheet, less the value of the scrap, divided by the number of parts from the sheet: ($28.27 - $0.966) / 64 parts = $0.427 per part.

Process cost per part. Next, we need to calculate the cost of the time needed to cut the parts from the sheet. Once it pierces the sheet, the laser can move through the steel at a speed of 0.989 ips. The perimeter of the blank and the circumference of the holes totals 26.21 inches. If it takes 2.5 seconds to pierce the steel, then the time needed to make this part is: (26.21 inches / 0.989 ips) + (8 x 2.5 seconds) = 46.5 seconds. Assuming the laser cutting machine costs $72 per hour to operate, the cutting process costs $0.93 per part.

Piece-part cost. Adding the process cost per part to the material cost per part, we get a piece-part cost of $0.427 + $0.93 = $1.357 per part.

Secondary processes. Now, we need to calculate the costs of the secondary operations needed to finish the part:

Now that we understand the costs associated with making this part, we can ask questions about the design and calculate the savings associated with those ideas:

Lean manufacturing has revolutionized how companies bring their products to market. But, while engineers have excelled at eliminating waste in the assembly process, they don’t always take an equally vigorous approach to the product itself. Designing a product for efficient manufacture and assembly can eliminate waste before the product even reaches the line.

It has long been established that 70 percent of a product’s cost is determined at the design phase. Once the product is being manufactured, engineers have few options to reduce costs without starting over.

Once production has begun, major design changes can incur not only large costs but also significant risk. Without an analysis of the design for manufacture and assembly (DFMA), production managers have difficulty knowing the financial impact of late-stage design fixes. And since there is an assembly already in production for which most costs are known, it’s much easier to look exclusively for savings through lean manufacturing.

In the long-term, however, this approach is problematic. Lean manufacturing, kaizen and Six Sigma are valuable techniques, but they do not address the causal relationship between part design and production efficiency.

Manufacturers also need a way to understand the cost trade-offs associated with changes in the product design, the manufacturing process, and the materials used to make each part. When this information is in the hands of engineers early in the design phase, they can make better decisions about costs. This is what a DFMA analysis provides.

DFMA is comprised of two parts. Design for assembly (DFA) is a quantifiable methodology for consolidating parts and simplifying the product. Design for manufacture (DFM) is a systematic approach to reducing costs by examining manufacturing processes and material choices.

A DFMA analysis early in the design stage can yield more savings than can lean manufacturing once the design is set and production is underway.

Description of the Problem

In the early stages of development, engineers are obsessed with satisfying functional requirements and are disengaged from the cost implications of their decisions. Some would argue that this uncompromising focus is appropriate, since the product has to meet the functionality demanded by customers. However, an overly isolated focus on function can cause teams to miss their target cost. Paradoxically, designing for cost and function at the same time allows manufacturers to build more performance into products for the same or lower price.Designing for function alone consumes large blocks of time in the development process, creating the perception that there is no time for anything else. However, studies have shown that an increase in time spent during the concept phases of product development-including a DFMA analysis-can actually shorten time to market.

An additional benefit of a DFMA analysis is that the design team understands costs before assembly begins, enabling them to make decisions that can influence the final cost of the product. In a more traditional development cycle, it’s less likely that they will be able to make changes later on.

For example, if a team designs a part to be produced by flame-cutting carbon steel and machining it to final shape, they will have few alternatives if they later discover that costs are too high. Tooling may have already been purchased, the supply chain established, and parts may even be rolling off the line.

In that situation, lean manufacturing looks like a good idea. With lean, the product design won’t change, so there is little risk in undertaking the effort. And simple changes in the process can have some benefit. Engineers can reduce setup and changeover time, switch to a more efficient supplier, or change sheet size and material usage.

But, if the design is scrutinized early in the development cycle, the engineering team might realize that forging the part to a near-net shape is much more cost-effective than cutting and machining it. Comparing the two processes is a fairly simple exercise during design, yet knowing which process makes the most sense financially is something most design teams struggle with.

It is important not only to understand the cost of a design, but the distribution of that cost as well. When design teams document this, they can focus their efforts to gain the greatest impact. Given that 75 percent of the cost of the part is in the material, looking for savings through improved setup is a relatively fruitless exercise. Setup consumes a small portion of the total cost.

While these principles hold true for components, the same ideas apply to whole products. About 70 percent of the total cost of most products is tied up in parts. The other 30 percent is labor and overhead.

Given this cost breakdown, it becomes obvious that a focus on the piece-part cost will have the most impact on the overall cost of the product. So while a discussion about manufacturing processes and material combinations for individual parts is essential, engineers should concentrate on simplifying their designs.

Product simplification can be defined as the challenge to come up with a design that meets the required functionality with the fewest parts. It can be accomplished using a classic DFA analysis. When applied at the early stages of design, DFA can have far-reaching impacts on cost.

Applying lean manufacturing to a product like the motor assembly in Fig. 1 could certainly have some effect on its cost. Fig. 2 shows how DFM and DFA analyses can simplify the product. Assuming both designs meet performance requirements, you can see how changes to the original design can have a bigger impact on cost than anything that could be achieved through lean manufacturing.

Comparing the two designs, the redesigned assembly has 12 fewer parts. That results in 12 fewer drawings and digital models to maintain, 12 fewer suppliers to qualify, 12 fewer service parts to consider, 12 fewer items to inventory, and so on. The redesign also costs 46 percent less.

In short, efforts to cut costs using lean have focused on the wrong area. To achieve the most impact, our efforts need to be pushed upstream to the design stage.

Early Cost Analysis

Engineering teams often don’t have a good handle on cost until the product is actually in production. To overcome that obstacle, design teams need tools to understand cost. Once they understand piece-part and labor costs, engineers can make changes to the product-when it’s still in the design phase-to cut costs and achieve profit targets.When they understand the costs on a product’s bill of materials, the design team can influence those numbers in three ways.

First, they can provide the supply chain group with the results of their cost modeling. This information is invaluable when negotiating with suppliers. No longer will the purchasing department need to send drawings to suppliers, wait weeks for quotes, try to make sense of the numbers, and finally select a supplier. Instead, prior to the quoting process, they will already know what the parts should cost. They can then use this information to make better buying decisions.

Second, if modeling indicates that product costs do not meet projected profit margins, the design team can use DFM techniques to investigate trade-offs at the piece-part level. Choices of manufacturing processes and material combinations, along with minor changes in the design of the individual parts, can have an impact on cost. Through early analysis, these outlays can be documented, and data-driven decisions can be made.

For example, let’s say a design called for a sand-casted metal part purchased through a domestic source at a cost of $4.81 per part. Then, to save money, the company opts to outsource the component to a low-cost region. Cost-modeling techniques allow us to challenge the choice of manufacturing process as well as the design of the component itself.

Through cost-modeling, we can see that die casting the part through a domestic source ($3.50 per part) is actually less expensive than sourcing a sand casting from a low-cost region ($3.82 per part). The next logical question is whether outsourcing the die casting would make even more sense. At first pass, it does, since a low-cost region can supply the part at $3.35 per piece.

However, these prices are just the cost to manufacture the part. Other costs need to be taken into account to make an apples-to-apples comparison between all the alternatives. Once logistics, shipping, communications and other costs are considered, it’s likely that sourcing the die casting from the low-cost region could not be justified. In the end, die casting the part through a domestic source makes the most economic sense.

The third way a design team can influence the costs on a bill of materials is to review the design of the product itself. The most effective way to reduce costs is to reduce the number of parts required for the product to accomplish its desired function. In addition to generating labor time estimates, a DFA analysis helps the design team determine a theoretical minimum part count.

To accomplish this, three questions are asked of each part to justify its being separate, by necessity, from all other parts in the product:

- Does the part have to be made of a different material?

- Does the part have to move with respect to other parts?

- Does the part have to be separate to avoid preventing assembly of other items?

DFA Index = (NM x 2.93)/TA.

In this equation, NM represents theoretical minimum number of parts, and TA stands for total operation time.

This index represents the efficiency of the design from an assembly perspective. It helps guide the team by comparing the part count in an existing design with what is possible to achieve. Generally, the higher the DFA Index, the better the design from a cost perspective.

DFA leads to dramatic savings and a more efficient manufacturing process that will ultimately result in more significant savings than could be achieved with lean manufacturing alone.

For example, consider the four designs in Fig. 3. The one on the far left is complex. Once in production, it will be difficult to produce cost-effectively. However, the three designs on the right have been progressively designed using DFA to be less expensive and easier to make. Once the design on the left is in production, no additional efforts can realistically come close to producing a product with a cost as low as one designed right the first time.

"Should-Cost" Example

Cost analysis is based on data related to families of compatible manufacturing processes and materials. Choosing an optimum manufacturing process from these family matchups entails the use of different, comparative cost models that reveal cycle times, material usage, scrap values, tooling costs, and other variables associated with each process.To see how this might work, let’s cost out a steel spacer plate. The square part is 4 inches wide, 4 inches tall, and 0.188 inch thick. It has a 1.75-inch diameter hole in the center and one 0.375-inch diameter hole in each corner. After a 1/4-20 self-clinching fastener is pressed into each corner hole, the assembly is powder-coated with a black finish.

Using established cost models, we can determine what the assembly should cost.

Weight. Let’s assume that this part will be laser-cut from a sheet of carbon steel and produced in an annual volume of 1,000 parts. Geometry and the density of the steel tell us that the blank weighs 0.851 pound. The material cut from the part weighs 0.151 pound, resulting in a part weight of 0.7 pound.

Cost of a sheet. Let’s assume this part will be cut from a 36- by 36-inch sheet. Allowing for 0.375 inch of clearance from part to part and from part to edge, we will get eight parts along the width of the sheet and eight parts along its length, or 64 parts in total.

We can calculate the weight of the sheet at 68.952 pounds. Assuming a cost of $0.41 per pound for the steel and a value of $0.04 per pound for the scrap left over from the sheet and for the holes cut from the part, we can calculate the cost of a sheet as $28.27.

Scrap value. The scrap from the sheet is the weight of the sheet less the weight of the 64 blanks cut from it: 68.952 pounds - (64 x 0.851 pound) = 14.488 pounds. The scrap from the holes is weight of the holes times the number of parts: 0.151 pound x 64 = 9.664 pounds. Thus, the total scrap produced from one sheet is 24.152 pounds. Given the scrap value of the material, we can calculate a scrap value of $0.966 from the sheet.

Material cost per part. The material cost per part is the cost of the sheet, less the value of the scrap, divided by the number of parts from the sheet: ($28.27 - $0.966) / 64 parts = $0.427 per part.

Process cost per part. Next, we need to calculate the cost of the time needed to cut the parts from the sheet. Once it pierces the sheet, the laser can move through the steel at a speed of 0.989 ips. The perimeter of the blank and the circumference of the holes totals 26.21 inches. If it takes 2.5 seconds to pierce the steel, then the time needed to make this part is: (26.21 inches / 0.989 ips) + (8 x 2.5 seconds) = 46.5 seconds. Assuming the laser cutting machine costs $72 per hour to operate, the cutting process costs $0.93 per part.

Piece-part cost. Adding the process cost per part to the material cost per part, we get a piece-part cost of $0.427 + $0.93 = $1.357 per part.

Secondary processes. Now, we need to calculate the costs of the secondary operations needed to finish the part:

- Each self-clinching fastener costs $0.25.

- Installing all four fasteners with a press takes 0.011 hour.

- Washing the part prior to painting takes 0.015 hour.

- Plugging the four fasteners prior to painting-and removing the plugs afterward-takes 0.02 hour.

- Painting the part 0.003 hour.

- Assuming a labor rate of $60 per hour, the total cost of the part is $1.357 + (4 x $0.25) + (0.049 hour x $60 per hour) = $5.297 per part.

Now that we understand the costs associated with making this part, we can ask questions about the design and calculate the savings associated with those ideas:

- Would replacing the self-clinching fasteners with tapped holes result in savings? It would eliminate the cost of inserting the fasteners.

- Would changing from carbon steel to stainless steel result in savings? It would eliminate the need to paint the part for corrosion resistance.

- Would changing from carbon steel to plastic result in savings? Would the investment in tooling for injection molding be offset by any process cost changes?

ASSEMBLY ONLINE

For more information on DFMA, visit www.assemblymag.com to read these articles:Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!