Reshoring Unpacked: A Transformational Shift From Global To Local

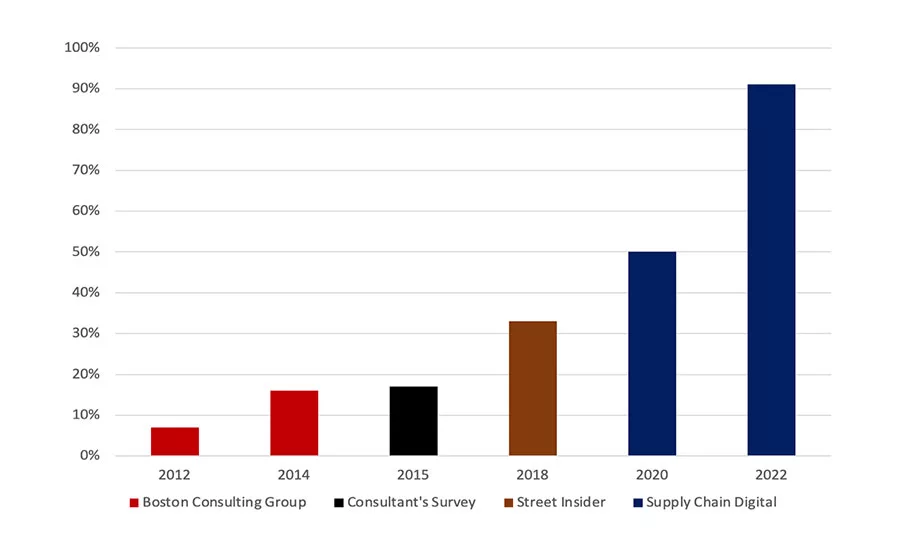

The Reshoring Initiative’s analysis of data from six surveys by five organizations over 10 years confirms that companies have actually the followed through on their reshoring job announcements. Source: Reshoring Initiative

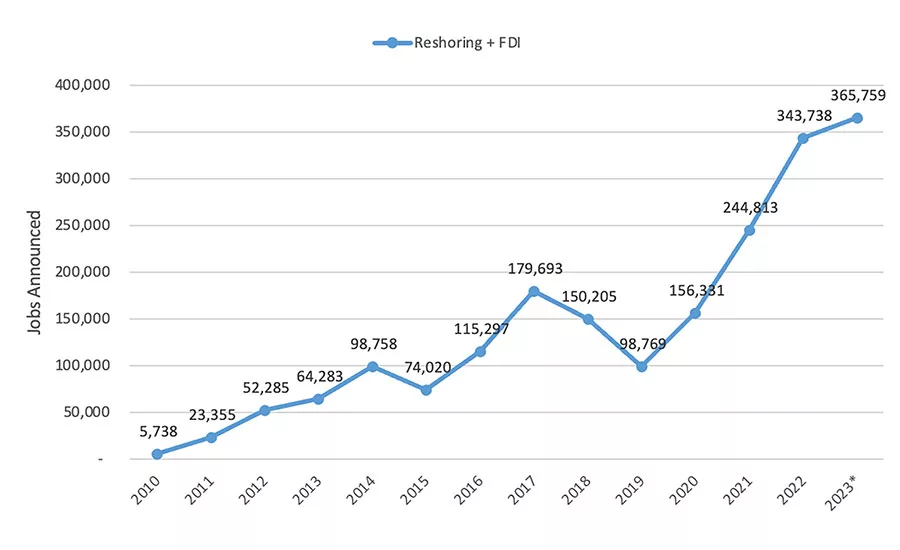

At the current rate, The Reshoring Initiative projects that there will be 1,614 cases of reshoring or FDI in 2023, resulting in 365,000 jobs. Source: Reshoring Initiative

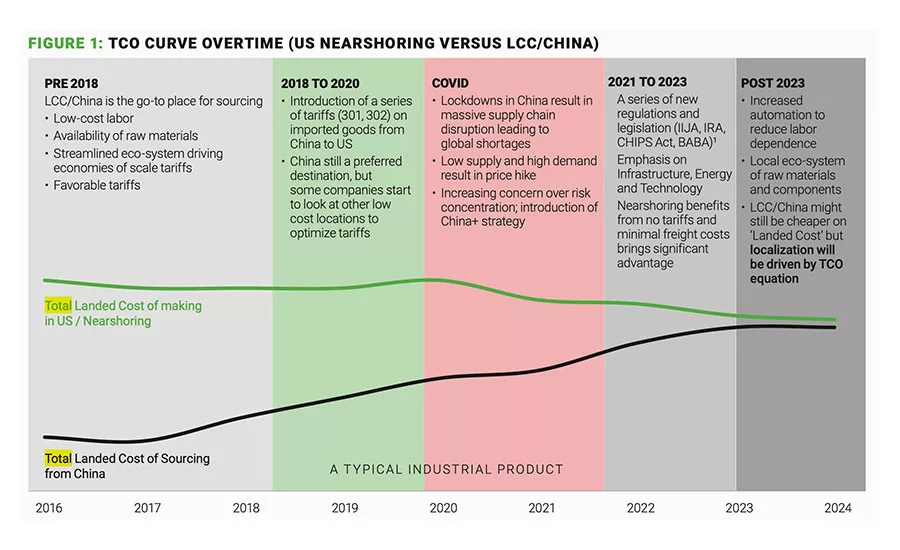

Markedly rising wages in China, increasing use of automation in the U.S., and new trade policies have reduced the total cost gap between Asian production and near-shoring to almost zero. Source: Alix Partners

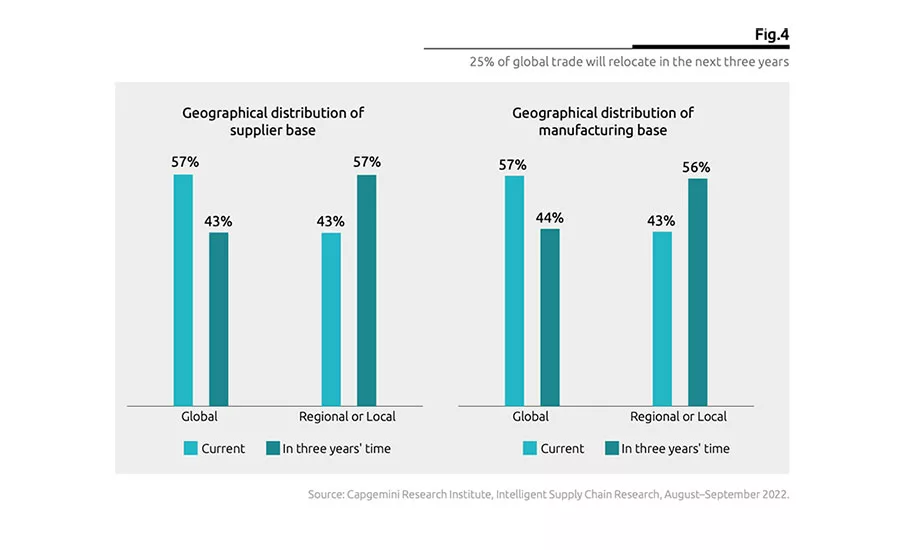

The geographic distribution of global suppliers will fundamentally shift from being mostly global to mostly local by 2026. Source: CapGemini

New research reveals that 25 percent of global trade will relocate within three years amid economic and geopolitical instability. The geographic distribution of global suppliers will fundamentally shift from being mostly global to mostly local by 2026.

A nationwide study of CEOs in 2022 found that 58 percent are considering reshoring. Forty-one percent estimate the timeframe to have operations fully reshored is one to three years. Similarly, a 2023 study of U.S. manufacturing executives by Forbes, Xometry and Zogby found that “82 percent of executives polled said they’d either moved overseas factories back home or were in the process of doing so.”

Are Companies Actually Reshoring?

The answer is clearly “yes.” Our own analysis of data from six surveys by five organizations over 10 years confirms that companies have actually the followed through on their reshoring job announcements. Our analysis has revealed an increase from 7 percent of companies reshoring in 2012 to 91 percent in 2022. Those results have a 97.4 percent correlation with the number of jobs created through reshoring or foreign direct investment (FDI) per year over the same time period.

According to the Reshoring Initiative’s report for the first half of 2023, reshoring and FDI job announcements have continued at a record-breaking run. Our data show 807 cases of reshoring and FDI with 182,000 jobs announced. If that rate continues, the projection for the entire year of 2023 is 1,614 cases and 365,000 jobs. The number of jobs announced in the first half of 2023 exceed the record number of jobs—340,000—announced in the same period in 2022.

The cumulative number of jobs announced since 2010 is now approximately 2 million—about 40 percent of what we lost to offshoring over the last 40 years.

Key Drivers of Reshoring

Reshoring’s shift into warp speed is attributed to more favorable U.S. industrial policy, greater geopolitical risk, and a better understanding of total cost of ownership (TCO).

U.S. policy has created favorable conditions for reshoring and FDI via the Infrastructure Investment and Jobs Act (IIJA), Inflation Reduction Act (IRA), and CHIPS and Science Act. Each act provides funding and tax incentives to spur domestic manufacturing in industries where the U.S. has an excess dependency on imports.

Looking for quick answers on assembly and manufacturing topics? Try Ask ASM, our new smart AI search tool. Ask ASM

Geopolitical disruptions are driving companies to re-evaluate supply chain priorities. COVID shutdowns, the war in Ukraine, the Israeli-Hamas conflict, and increasing tension over Taiwan show that it is time for companies to consider reshoring and near-shoring as “insurance” against catastrophic disruptions.

TCO analysis is helping companies see that reshoring is economically feasible in about 25 percent of cases. Markedly rising wages in China, increasing use of automation in the U.S., and new trade policies have reduced the total cost gap between Asian production and near-shoring to almost zero.

Comparative Analysis

TCO is the best metric to use for comparative analysis. The Reshoring Initiative’s TCO Estimator is a free online tool that helps companies account for all factors to compare the true total cost of domestic and offshore sourcing and siting. These factors include overhead, balance sheet, risks, corporate strategy, and other external and internal business considerations. The impact of using TCO shows that shifting decisions from a price basis to TCO can be expected to drive reshoring of 20 to 30 percent of what is now imported.

Are you thinking about reshoring? For help, call 847-867-1144 or email harry.moser@reshorenow.org. Our mission is to get companies to do the math correctly using our TCO Estimator. By using TCO, companies can better evaluate sourcing, identify alternatives and even make a case when selling against offshore competitors.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!