ASSEMBLY Capital Spending Report: Capital Spending to Increase

With automotive and aerospace manufacturing going strong, our annual Capital Equipment Spending Survey predicts continued growth in investment.

The automotive industry continues to drive growth in capital equipment spending. Transportation equipment manufacturers will account for 30 percent of total spending next year. Photo courtesy Faurecia

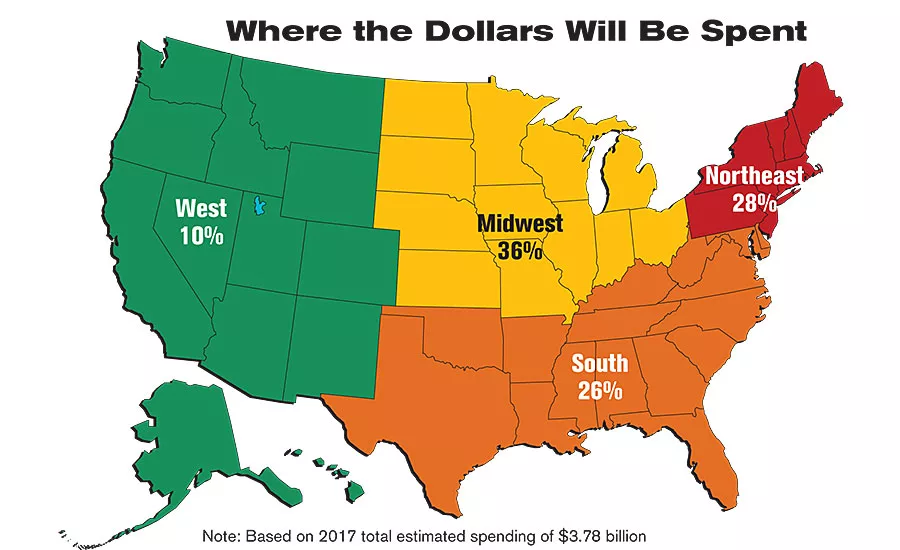

The Northeast will account for 28 percent of total spending this year. That’s the highest share for the region since 2012.

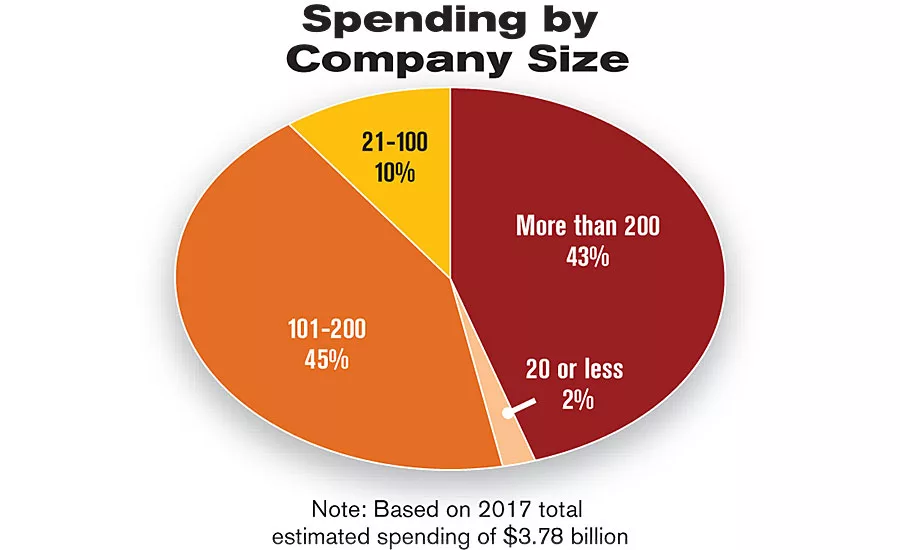

As usual, the country’s largest assembly plants have the deepest pockets and the rosiest outlook. Companies with more than 100 workers will account for 88 percent of total spending next year.

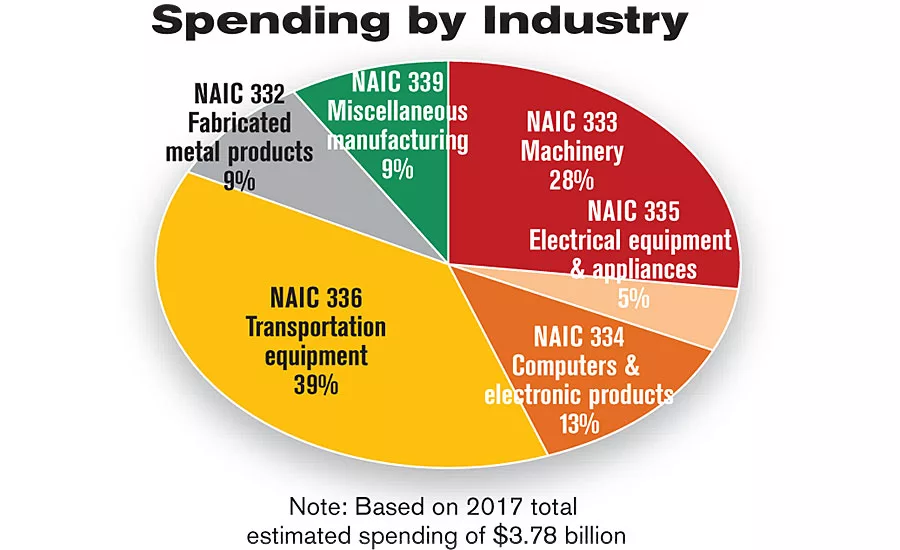

For the seventh time in the past decade, transportation equipment manufacturers will spend more on assembly technology than any other industry.

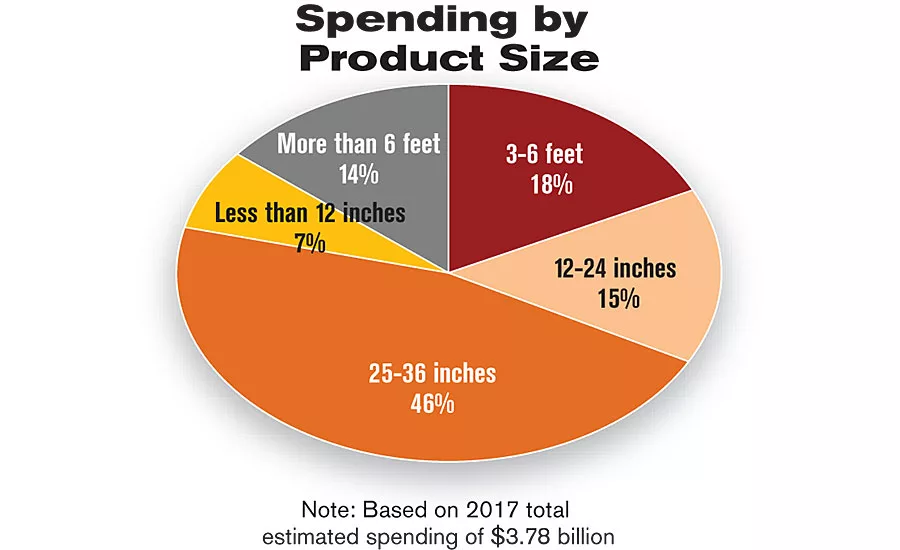

Manufacturers of small products (anything that can fit inside a 12-inch cube) will account for just 7 percent of total spending next year— the smallest share for that segment in the survey history.

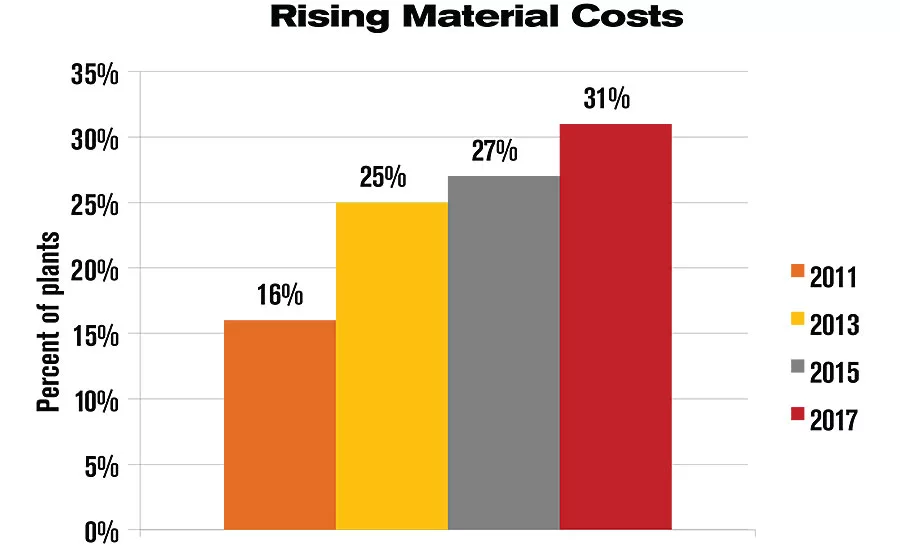

Thirty-one percent of plants will buy equipment next year to mitigate material costs. That’s the highest percentage in the history of our survey.

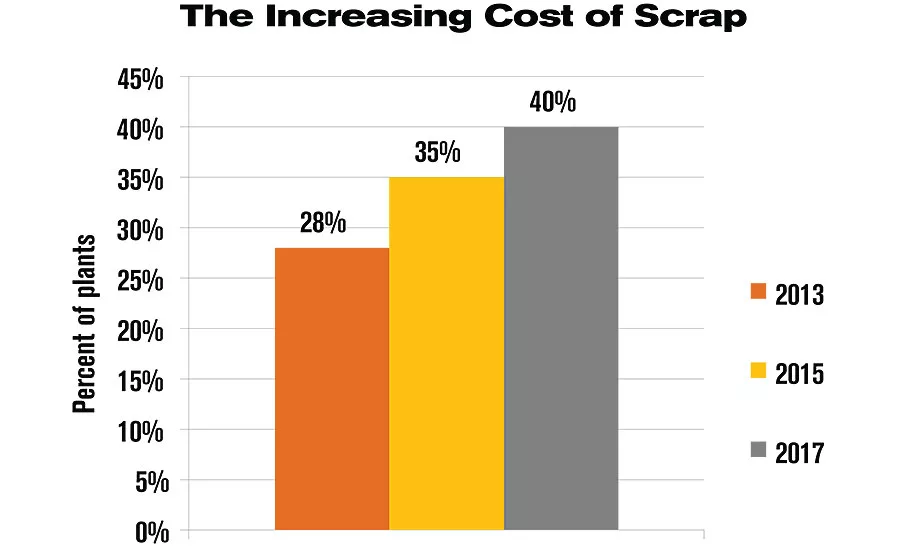

Assemblers are increasingly concerned about the cost of scrap. Next year, 40 percent of plants will buy equipment to lower scrap costs, the most since 2013.

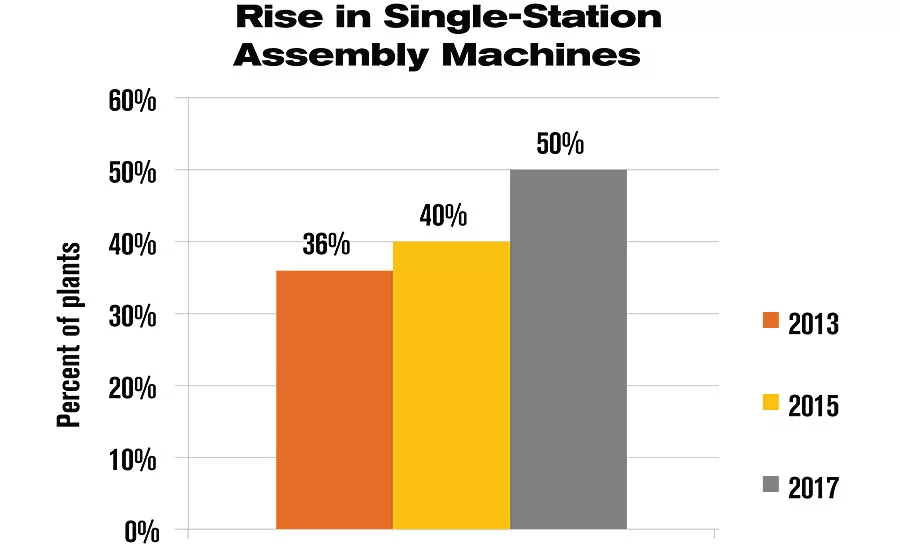

Assemblers are increasingly investing in single-station assembly machines: presses, automatic riveters, and automatic screwdriving equipment. Fifty percent of plants will purchase such equipment next year, the most since 2011.

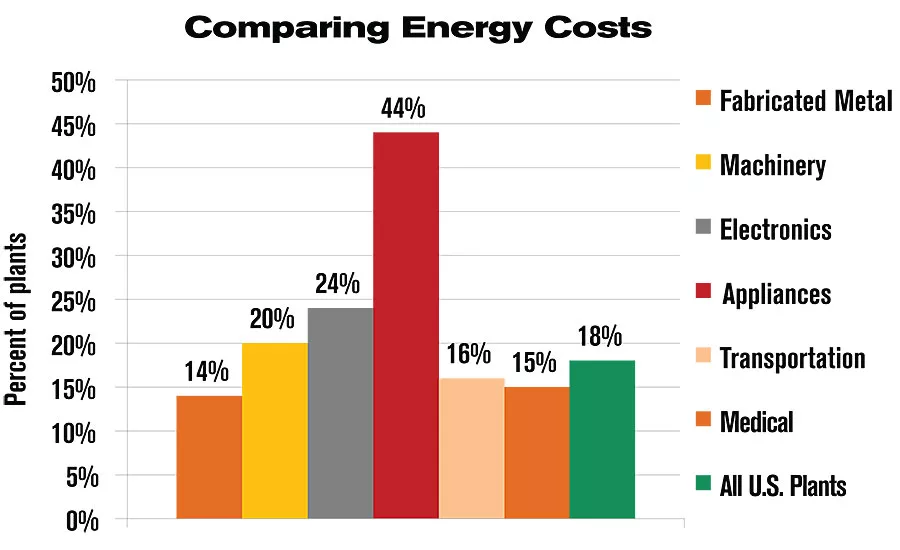

For the first time this year, we asked about energy costs. One industry stood out: 44 percent of manufacturers of appliances and electrical equipment said that they were buying equipment to reduce their energy costs. That’s more than twice the percentage for all U.S. factories.

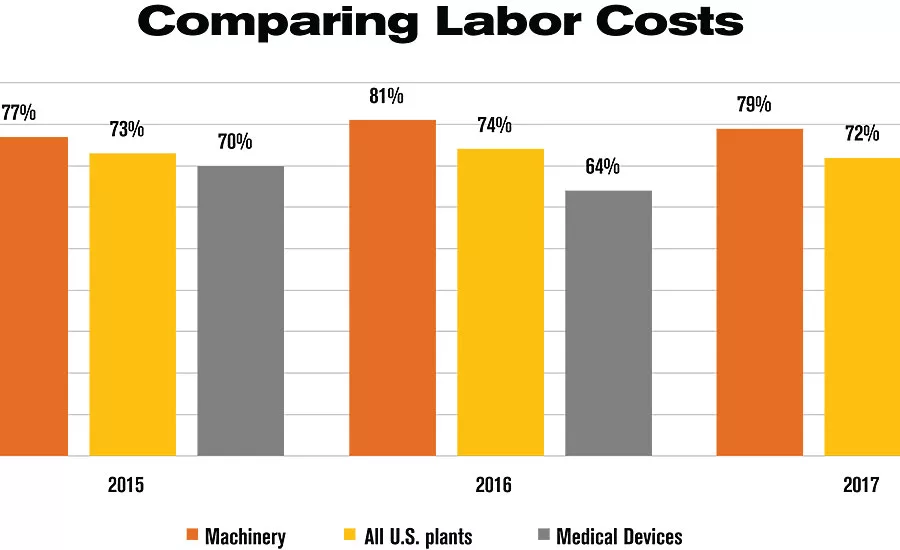

Over the past three years, machinery manufacturers have been more concerned about labor costs than other manufacturers. Next year, 79 percent of machinery makers will buy equipment to reduce labor costs, compared with 72 percent for all U.S. plants. In contrast, medical device manufacturers have been less concerned about labor costs.

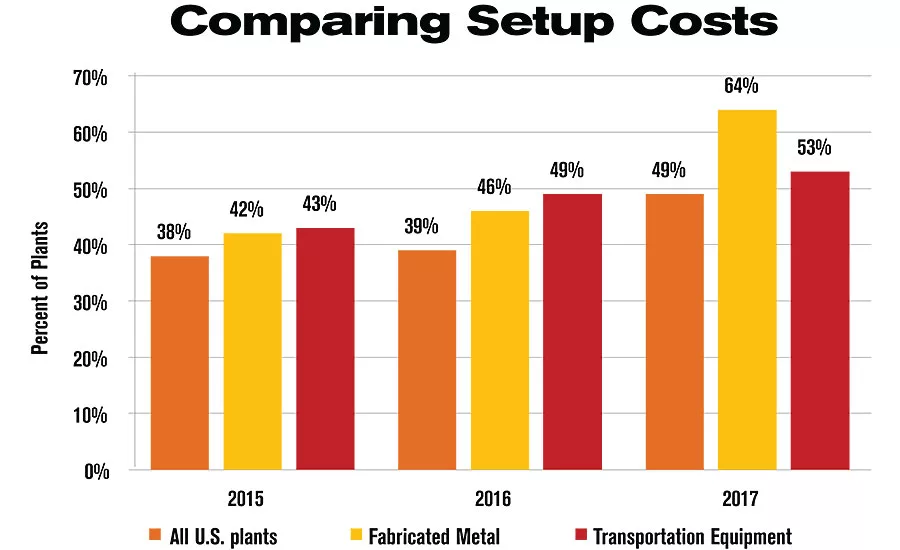

Compared with other industries, manufacturers of fabricated metal products and transportation equipment are more concerned about indirect labor costs, such as setup and maintenance. Next year, 64 percent of fabricated metal products factories and 53 percent of transportation equipment factories will invest in equipment to reduce indirect labor costs. Both percentages are higher than the national ratio.

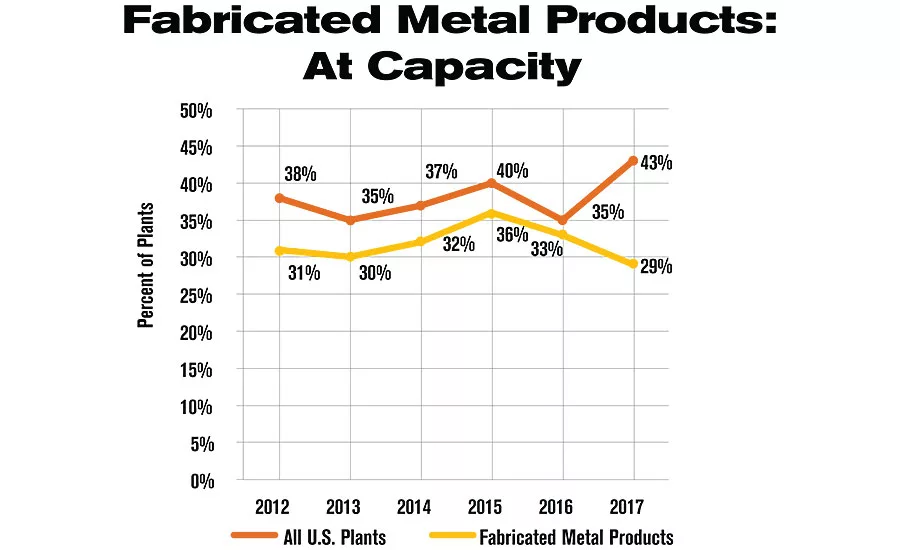

Compared with other industries, manufacturers of fabricated metal products seem to have plenty of capacity. Only 29 percent of plants in this industry will buy equipment next year to increase capacity. That’s well below the national percentage. In fact, the industry has been below the national percentage for the past six years.

Only 16 percent of respondents will spend less in 2017 than they did 2016—an all-time low for our survey.

Overall, 2016 has been a pretty good year for U.S. manufacturing. In every industry covered by ASSEMBLY magazine, manufacturers were investing in people, plants and equipment.

Here are just some of the manufacturing headlines from the past year:

FCA US announced plans to invest $1.48 billion in its assembly plant in Sterling Heights, MI, to build the next generation Ram 1500 truck.

Whirlpool Corp. started a $40 million expansion project at its dishwasher assembly plant in Findlay, OH. The project will add 86,400 square feet to the facility and create approximately 50 new jobs. In addition, the appliance manufacturer completed work on a multimillion-dollar expansion project at its assembly plant in nearby Greenville, OH.

UTC Aerospace Systems began building an 80,000-square-foot assembly plant in Foley, AL, to supply parts for Airbus’ assembly plant in nearby Mobile. Slated to open in 2017, the factory is expected to create 260 jobs.

Medical device manufacturer Becton Dickinson & Co. is investing $100 million to expand its assembly plant in Holdrege, NE, to make insulin syringes.

Manufacturers had good reason to build in 2016. According to commercial real estate services firm Cushman & Wakefield, the vacancy rate for industrial properties in the U.S. reached a 15-year low in 2015.

Manufacturing employment more or less held steady this year. According to the latest figures from the Labor Department, U.S. manufacturers employed 12.26 million people through October 2016. That’s down a bit from the 12.31 million employed in October 2015, but it’s still 805,000 more manufacturing jobs than there were in March 2010, the low point of the Great Recession.

Looking for quick answers on assembly and manufacturing topics? Try Ask ASM, our new smart AI search tool. Ask ASM

And, the Institute for Supply Management’s manufacturing index registered 51.9 in October. Anything higher than 50 signals growth, and the index has averaged 50.6 for the past 12 months.

Continued Growth

With the economy humming, manufacturers should continue investing in capital equipment next year, and the results of our 21st annual Capital Equipment Spending Survey indicate that manufacturers will increase spending on assembly technology in 2017.

Specifically, U.S. assembly plants will spend $3.78 billion on new equipment in 2017, an increase of 8 percent from the $3.5 billion projected to be spent in 2016.

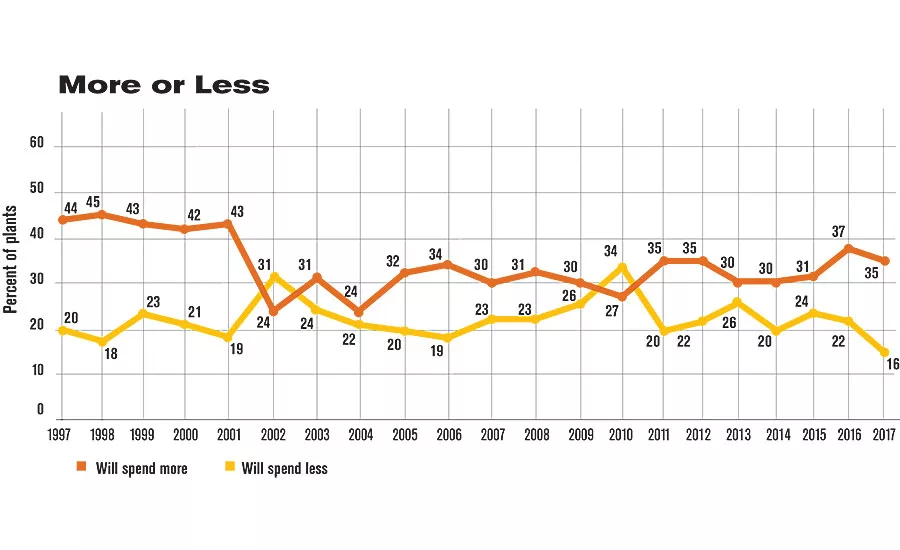

Some 35 percent of respondents will spend more on assembly technology next year than they did this year. That marks the seventh straight year that the “we’ll spend more” percentage has been above 30 percent. Forty-nine percent will spend the same as they did in 2016, and only 16 percent of respondents will spend less in 2017 than they did 2016. The latter figure is an all-time low for our survey.

On average, manufacturers will spend $273,108 on assembly technology in 2017, and that is lower than the $298,630 average budget for 2016. On other hand, the median budget figure is up: from $30,000 in 2016 to $50,000 in 2017.

Aggregate budget data indicate a healthy increase in spending for 2017. For example, 22 percent of plants have capital budgets of at least $500,000. That’s nearly double the figure for 2016, and it’s the highest percentage since 2009. At the same time, 18 percent of plants will spend between $100,000 and $500,000 next year, compared with 16 percent in 2016. Only 60 percent of plants will spend less than $100,000 next year, the lowest percentage in five years.

Regardless of how much they spend on capital equipment next year, assemblers continue to expect a quick return on investment (ROI). Next year, 25 percent of plants have an ROI period of less than 12 months—the highest percentage since 2004. At the same time, only 35 percent of plants have an ROI period of at least two years. That marks the seventh straight year in which that percentage has been 35 percent or less.

ROI is less of a concern in the transportation equipment industry. Thirty-nine percent of transportation equipment assemblers can afford to wait two years or more for ROI, the second straight year in which that percentage has been above the national figure. That makes sense. Base vehicle designs typically last a few years before OEMs hit the reset button. Aircraft designs last even longer.

On the other hand, ROI is more of a concern in the fabricated metal products industry. Thirty-four percent of plants in this industry have an ROI period of less than a year. It’s the second straight year that the fabricated metal products industry has led the nation in that percentage. This may due to shorter product runs or higher wear and tear on welding equipment, robots, tooling and other fabrication technology.

It remains to be seen how tax law changes will affect ROI. Last year, Congress changed the rules for “bonus depreciation.” The tax code allows manufacturers to write off the value of an asset over time. Bonus depreciation is an additional amount of depreciation that can be deducted in the first year of operation for the deductible equipment or machinery. The goal was to incentivize manufacturers to spend more than $2 million in capital investment. Bonus depreciation will remain at 50 percent in 2016 and 2017, but then go to 40 percent in 2018 and 30 percent in 2019.

Spending Motives

Replacing old equipment continues to be a priority for ASSEMBLY’s readers. For the fourth time in the past six years, replacing old or worn out equipment is the No. 1 reason for investing in assembly technology. Some 47 percent of respondents plan to replace old tools and machines in 2017. That figure has been above 46 percent only four times in the past 13 surveys, but two of those were recorded in the past three years.

Perhaps manufacturers postponed replacing capital equipment during the Great Recession and are now in dire need of new machinery. The problem is particularly acute among manufacturers of medical devices and transportation equipment. Fifty-three percent of medical device manufacturers and 61 percent of transportation equipment manufacturers will replace old machinery next year, marking the third straight year that those two industries have led the nation in that statistic.

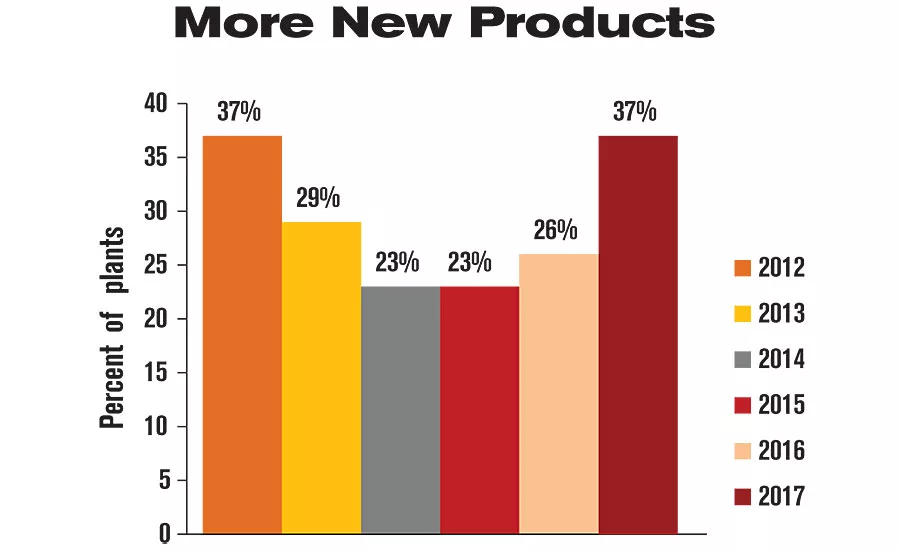

Here’s an encouraging number from this year’s data: 37 percent of plants will buy equipment next year to assemble a new product. That figure had been below 30 percent in the past four surveys.

One might expect that medical device manufacturers would be leading the charge in new product development, but only 33 percent of assemblers in that industry will buy equipment next year to assemble a new product, the second lowest percentage of any industry this year. In fact, medical device manufacturers have been below the national figure in new-product-related investment for seven straight years.

So which industry is constantly generating new products? How about transportation equipment manufacturing? Thirty-nine percent of manufacturers of cars, trucks, aircraft and motorcycles will be purchase equipment next year to make new things, the 11th straight year in which that industry has been above the national figure.

Lean manufacturing is becoming less important as a reason for capital investment. Only 16 percent of plants will buy equipment next year to implement lean manufacturing. That compares with 18 percent in 2016, and it’s an all-time low for our survey. Of course, after taking the manufacturing world by storm back in the ’90s, lean is standard operating procedure for most assemblers today. Manufacturers may not have to get lean—they already are.

On the other hand, quality—the roof of the house of lean—may be increasing in importance. Nineteen percent of assembly plants will invest in technology to improve product quality next year. That compares with 17 percent in 2016, and it’s an eight-year high.

Given the recall disasters in the automotive industry during the past few years, it’s not surprising to note that 22 percent of transportation equipment manufacturers—more than any other industry—will be buying equipment to improve product quality. In fact, transportation equipment manufacturers have led all industries in quality investments for the past four years.

According to latest figures from the Federal Reserve, U.S. manufacturing operations were running at 74.9 percent of capacity in October. That compares with 75.6 percent in October 2015 and the 10-year low of 63.8 percent in 2009.

Given the amount of untapped capacity out there, only 35 percent of plants will buy equipment next year to increase capacity or assemble higher volumes of existing products. That compares with 43 percent in 2016, and it’s the lowest since 2013.

Compared with other industries, manufacturers of fabricated metal products seem to have plenty of capacity. Only 29 percent of plants in this industry will buy equipment next year to increase capacity. That’s well below the national percentage, and it ties an all-time low for this industry. In fact, the fabricated metal products industry has been below the national percentage for the past six years.

In contrast, 44 percent of medical device manufacturers—more than any other industry—are investing in equipment to boost capacity. It’s the third time in four years that that figure has been above 42 percent.

Other motives for buying equipment include:

- cost reduction, 44 percent.

- reduce cycle time or eliminate a bottleneck, 31 percent.

- increase safety, 20 percent.

- keep up with competition, 14 percent.

- meet OEM or downstream requirements, 10 percent.

- comply with standards or industry regulations, 9 percent.

Labor Costs

As always, the top two targets for cost reduction are direct labor and indirect labor. However, the latter is increasing in importance relative to the former.

Some 72 percent of plants are looking to decrease direct labor costs next year. That’s still No. 1, but five years ago, that figure was 76 percent and 10 years ago, it was 83 percent.

That makes sense. Wage growth in manufacturing—and, indeed, the entire economy—has essentially been stagnant, despite the economic recovery. According to the Bureau Labor Statistics, wages for U.S. production workers increased just 2.4 percent from October 2015 to October 2016. That’s well short of the Federal Reserve’s target of 3.5 to 4 percent for nominal wage growth (assuming 2 percent inflation target, 1.5 percent productivity growth, and a stable labor share of income).

Not surprisingly, machinery manufacturers are more concerned about labor costs than other industries. Producing large, complex assemblies in relatively low volumes is not conducive to labor-saving automation. Thus, 79 percent of machinery manufacturers—the highest ratio of any industry—are looking to lower labor costs.

In contrast, medical device manufacturers have been less concerned about labor costs. Only 68 percent of plants in that industry are targeting labor costs next year, marking the third straight year that this industry has been below the national figure. That makes sense, too. Medical devices tend to be small, high-value products produced at high volumes, which makes them ideal candidates for automated assembly.

If assemblers are less concerned about the cost of direct labor, they are more worried about the cost of indirect labor. Nearly half (49 percent) of respondents are looking to reduce setup, maintenance and other indirect labor costs next year. That compares with 34 percent in 2014 and 39 percent in 2016, and it’s the highest percentage since 2001.

Compared with other industries, manufacturers of fabricated metal products and transportation equipment are more concerned about indirect labor costs, such as setup and maintenance. Next year, 64 percent of fabricated metal products factories and 53 percent of transportation equipment factories will invest in equipment to reduce indirect labor costs. Both percentages are higher than the national ratio, and they have been for the past three years.

Cut the Scrap

Forty percent of respondents are looking to reduce the cost of scrap. That compares with 35 percent in 2015 and 28 percent in 2013, and it’s the highest percentage since 2010.

Of course, the best way to reduce scrap costs is not to produce any. To that end, assemblers will be investing heavily in test and inspection technology next year.

Fifty percent of U.S. assembly plants will purchase vision systems, sensors and other inspection technologies next year. That percentage has been at least 48 percent for five straight years, and inspection technology is now regularly among the top five most popular item on manufacturers’ wish lists.

All totaled, sales of inspection equipment will increase 14 percent, from $212 million in 2016 to $241.7 million in 2017.

The biggest markets for inspection technology next year will be computers and electronics, fabricated metal products, transportation equipment, and appliances.

Such projections bode well for a technology that enjoyed a banner year in 2015. North American sales of machine vision components and systems grew to $2.3 billion last year, the highest annual total on record, according to statistics issued by AIA, the industry’s trade group. (2016 data was not available at press time.)

“Interest in vision and imaging technology is at an all-time high today,” says AIA President Jeff Burnstein. “We continue to see new and exciting applications emerge for vision in all aspects of automation. Imaging technology is being used more and more outside the factory as well, with growth in areas like life sciences and unmanned aerial vehicles. It is an exciting time to be involved in this industry.”

Test equipment should also see a boost in sales next year. Fifty percent of plants—the highest ratio in eight years—will buy leak testers, functional testers, electrical testers and other equipment in 2017. Sales of test equipment will increase 8 percent, from $245 million in 2016 to $264.6 million in 2017.

Sixty-four percent of machinery manufacturers will buy test equipment next year, more than any other industry. Transportation equipment manufacturers are a close second—55 percent of plants in this industry will buy test equipment in 2017.

That would mesh with what other analysts are predicting. For example, market research firm Technavio expects the worldwide market for test and measurement equipment to increase 5 percent annually through 2020. Demand will be particularly strong in the automotive, telecommunications and aerospace and defense industries.

Other Cost Targets

As manufacturers increase their consumption of exotic materials, such as composites and titanium, a growing number are concerned over the cost of those materials. Thirty-one percent of assembly plants are looking to lower their material costs next year. That’s a record high, and it’s the fifth straight year in which that percentage has been above 25 percent.

Material costs are particularly concerning to manufacturers of electrical equipment and appliances, transportation equipment, and medical devices. In fact, material costs have been a concern for 30 percent or more of medical device assemblers for four consecutive years.

For the first time this year, we asked whether energy costs would be a target of capital investment, and only 18 percent of plants said they would be buying equipment to lower their energy bills. Manufacturers of computers and electronics (24 percent) are particularly keen to lower their energy costs, which makes sense since machines such as reflow ovens and X-ray inspection machines consume a fair bit of electricity.

Less understandable is that 44 percent of appliance and electrical equipment assemblers—double the percentage of any other industry—say they will be targeting energy costs next year. Such a high figure could be attributable to a relatively small sample size for the industry this year. Or, it could reflect a prevalence of relatively energy-intensive processes, such as powder coating, epoxy curing and resistance welding.

Only 12 percent of plants are looking to lower their warranty and field-service costs next year—the same percentage as 2016. Not surprisingly, appliance and transportation equipment manufacturers are more concerned about warranty costs than other industries.

New vs. Used

Assemblers continue to stretch their capital budgets with used or rebuilt equipment. Next year, manufacturers will meet, on average, 39 percent of their assembly technology needs with used or rebuilt equipment. That’s up from 37 percent in 2016.

It wasn’t always that way. From 1997 to 2000, for example, manufacturers met, on average, less than 25 percent of their assembly technology needs with used machinery. But, recessions and outsourcing have certainly taken their toll on domestic manufacturers, and plenty of quality used equipment—robots, welders, indexers, crimping presses, and all manner of machine tools—is available at bargain prices.

Historically, manufacturers of fabricated metal products, transportation equipment, and computers and electronics are more likely to purchase used or rebuilt equipment, while manufacturers of medical devices are less likely.

Not surprisingly, small companies are more likely than large ones to purchase new equipment. For example, companies with 20 employees or less will meet, on average, 51 percent of their technology needs with used or rebuilt equipment next year. In fact, over the past four years, that ratio has never been less than 42 percent. In contrast, companies with 200 or more employees will meet, on average, just 18 percent of next year’s technology needs with “previously owned” equipment.

Assembly DIY

Last October’s ASSEMBLY Show featured numerous suppliers of modular machine components and framing systems, including Bosch Rexroth, Creform, Item and Flex Craft. And why not? Next year, assemblers will meet, on average, 42 percent of their assembly technology needs with equipment built in-house. In fact, that percentage has been over 40 percent for 11 of the past 16 years.

Many assemblers are doing more than just building part racks and workstations, too. Twenty or thirty years ago, designing and building an automated assembly system required time, resources and a certain amount of arcane knowledge. Today, creating simple automated assembly cells is well within the capability of even the most harried engineering department. Robots have become less expensive and easier to use. Prepackaged XYZ motion control systems and servo-driven indexers are now widely available from many suppliers.

Historically, manufacturers of appliances and electrical equipment are more likely than other industries to build in-house equipment. In 2017, makers of dryers, transformers and other products will meet, on average, 47 percent of their technology needs with in-house equipment. In contrast, electronics assemblers are the least likely to go the DIY route. Next year, manufacturers of computers and electronics will meet, on average, 35 percent of their technology needs with in-house equipment.

Ironically, large manufacturers are much less likely to build in-house equipment than smaller ones, despite the greater number of personnel. Companies with 200 or more employees will meet, on average, just 30 percent of their technology needs with in-house equipment. In fact, companies with at least 200 employees have been below the national average in terms how much of their equipment is built in-house for at least the past seven years.

As with used equipment, it’s the smallest manufacturers that have the greatest inclination toward DIY. Next year, companies with 20 employees or less will meet, on average, 53 percent of their technology needs with in-house equipment. That’s up from 45 percent in 2016 and it’s the highest percentage in four years.

Automating to Compete

Manual assembly remains the most popular way to put together a product. Some 87 percent of respondents employ at least some manual operations to assemble their products. That figure has remained constant for the past 21 years, and it’s not all that surprising. After all, people are the most flexible assembly machines.

However, there’s no question manufacturers are looking to automate where they can. Some 68 percent of respondents say they employ semiautomatic equipment at their assembly plants. That’s up from 61 percent last year, and it’s the highest percentage since 2012. (We define semiautomatic equipment as machinery that combines manual and automatic processes, such as an autofeed screwdriver or a standalone riveting cell.)

Historically, manufacturers of computers and electronic products are more likely than other industries to employ semiautomatic equipment, while machinery manufacturers are less likely.

Even semiautomatic equipment is seemingly out of reach of smaller companies, however. Eighty percent of companies with 101 to 200 workers employ semiautomatic equipment, and 74 percent of companies with more than 200 workers use such machinery. In contrast, only 59 percent of companies with 21 to 100 workers use semiautomatic equipment.

Be that as it may, we expect demand for semiautomatic, single-station assembly machines to increase significantly next year. Fifty percent of plants will invest in presses, riveters or automatic screwdriving systems next year. That’s up from 44 percent in 2016, and it’s the most since 2011.

Demand for single-station assembly machines should be particularly strong among transportation equipment manufacturers (63 percent), appliance manufacturers (63 percent), and fabricated metal product manufacturers (57 percent).

All totaled, manufacturers will spend $489.4 million on single-station assembly systems in 2017, a 22 percent increase from 2016.

Among single-station assembly equipment, demand for presses will be particularly strong. Thirty-three percent of plants will invest in pneumatic, hydropneumatic and electric assembly presses next year. That compares with 26 percent in 2016 and 23 percent in 2015.

An increase in semiautomatic production will not come at the expense of fully automatic assembly. Indeed, 24 percent of plants will buy multistation automated assembly systems next year. That compares with 21 percent in 2016 and 16 percent in 2015, and it’s the highest percentage since 2010.

Much of the demand for automated assembly systems is coming from manufacturers of medical devices and electrical equipment.

All totaled, manufacturers will spend $750 million on multistation automated assembly systems in 2017, up 7 percent from 2016.

The increased demand for automated assembly systems will spark sales of related technologies, as well. For example, 22 percent of plants will buy bowl feeders, tray feeders and other parts feeding technologies next year, up from 19 percent in 2016 and the most since 2012. Similarly, 21 percent of plants will invest in indexers, linear actuators and other motion control technology in 2017. That compares with 19 percent in 2016, and it’s the highest percentage since 2007.

In all, manufacturers will spend $69.5 million on part feeders next year (a 16 percent increase) and $94 million on motion control technology (an 8 percent increase).

What Assemblers Want

As usual, power tools will be the No. 1 item on assemblers’ shopping lists next year. Some 68 percent of assembly plants will purchase impact wrenches, cordless screwdrivers, DC electric nutrunners, handheld riveters and other power tools in 2017, compared with 62 percent in 2016. Demand will be particularly strong among manufacturers of transportation equipment and fabricated metal products.

All totaled, assemblers will spend $234.7 million on tools next year, or 20 percent more than they spent in 2016.

Another technology that should enjoy an increase in demand is automated dispensing equipment, particularly among manufacturers of machinery, transportation equipment and appliances. Twenty-six percent of plants will purchase handheld time-pressure dispensers, meter-mix systems and other dispensing technology next year. That compares with 19 percent in 2016, and it’s the most since 2011.

All totaled, spending on dispensing equipment should increase 2 percent, from $133.5 million in 2016 to $136.1 million in 2017.

The biggest decrease in demand will be for computers and software. Sixty percent of plants will buy design analysis software, manufacturing execution systems, statistical process control software and other information technology next year, compared with 62 percent in 2016.

However, assemblers will dedicate an average of 10 percent of their 2017 budgets to computers and software, down from 13 percent in 2016. That translates into a 17 percent decrease in total spending on the technology, from $356.7 million in 2016 to $296 million in 2017.

Our survey results also indicate a potential decrease in demand for conveyors and material handling equipment. Twenty-five percent of plants will invest in conveyors next year, which is up from 23 percent in 2016. However, on average, assemblers will dedicate only 2 percent of their budgets to material handling technology. That’s down from 3 percent in 2016 and it’s the lowest average in five years.

That reduction will translate into a 28 percent decrease in total spending on conveyors, from $105 million in 2016 to $75.6 million in 2017.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!