ASSEMBLY Capital Spending Report 2017: Capital Spending Continues to Increase

With the economy firing on all cylinders, our annual Capital Equipment Spending Survey predicts continued growth in investment.

Transportation equipment assemblers will spend, on average, $2.3 million on assembly technology next year. Photo courtesy BMW

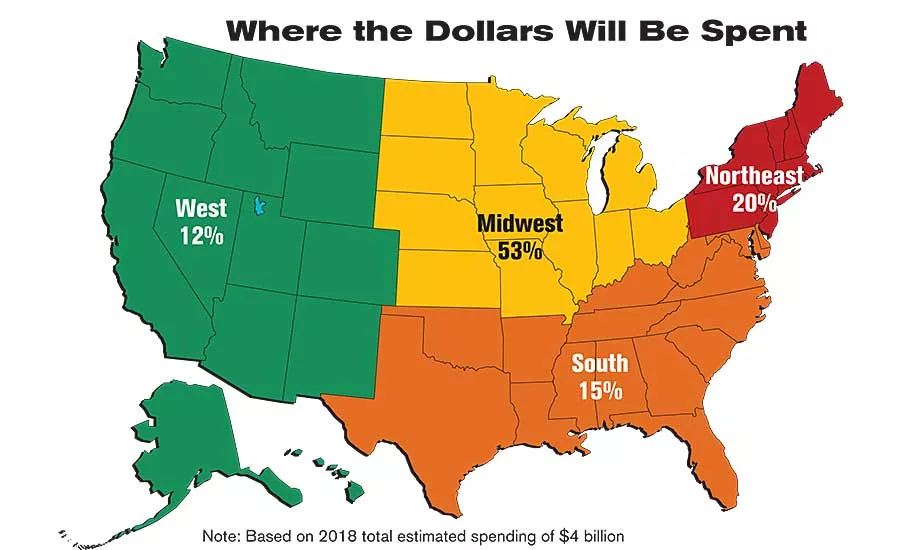

The Midwest will account for 53 percent of all spending on assembly technology next year. That’s the largest percentage for the region since 2013.

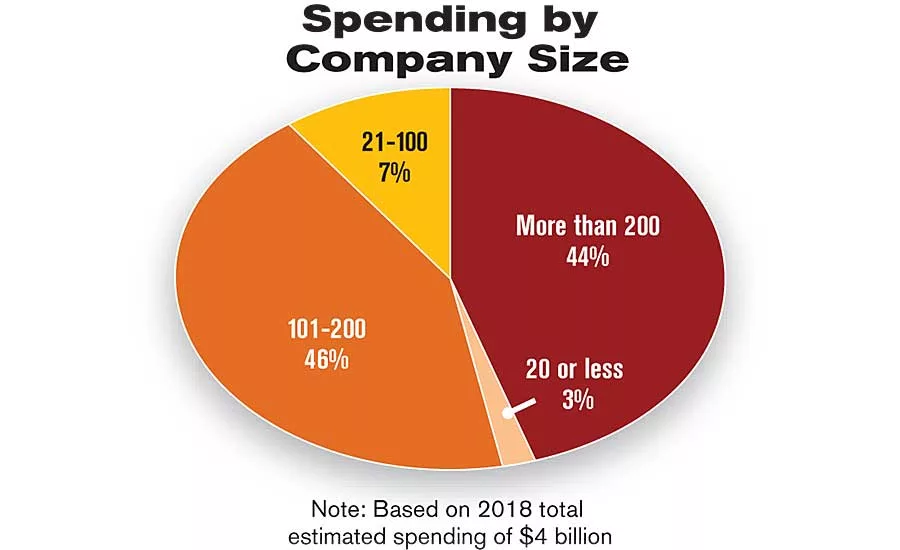

For the second straight year, midsized companies—those with 101 to 200 employees— will account for the lion’s share of total spending on assembly technology.

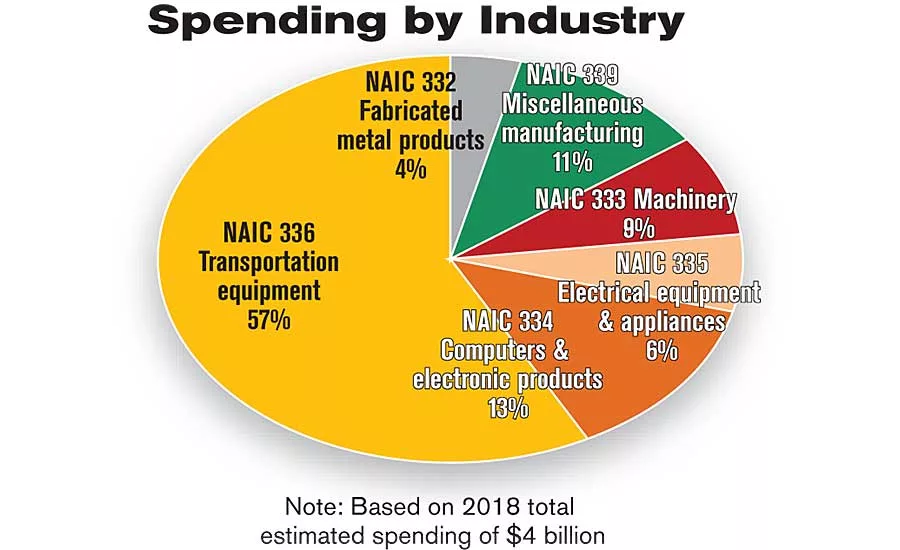

The fabricated metal products industry will account for just 4 percent of total spending in 2018. That’s the lowest share for the industry in survey history.

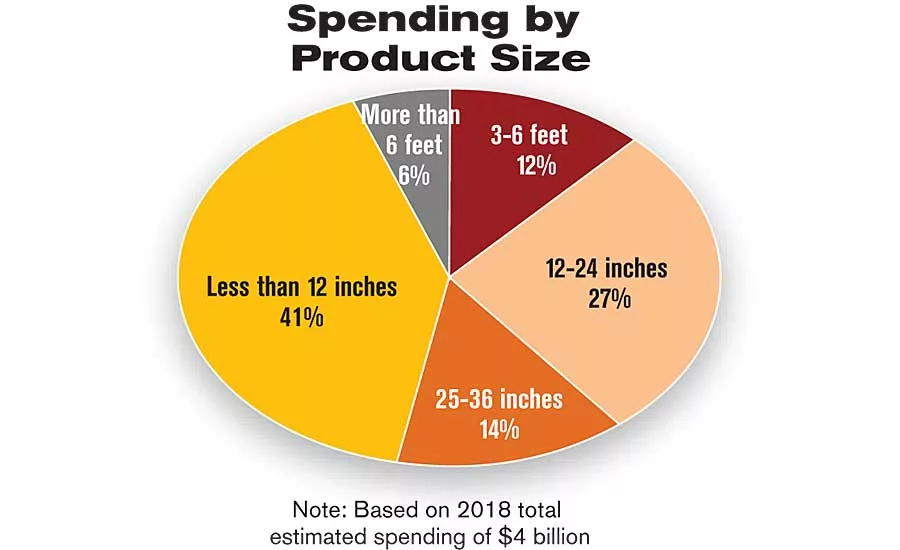

Assemblers of products that can fit inside a 12-inch cube will represent 41 percent of total spending next year. That’s the most for this category since 2014.

One-third of assembly plants are looking to lower material costs next year. That’s a record high, and it’s the sixth straight year in which that percentage has been at least 25 percent.

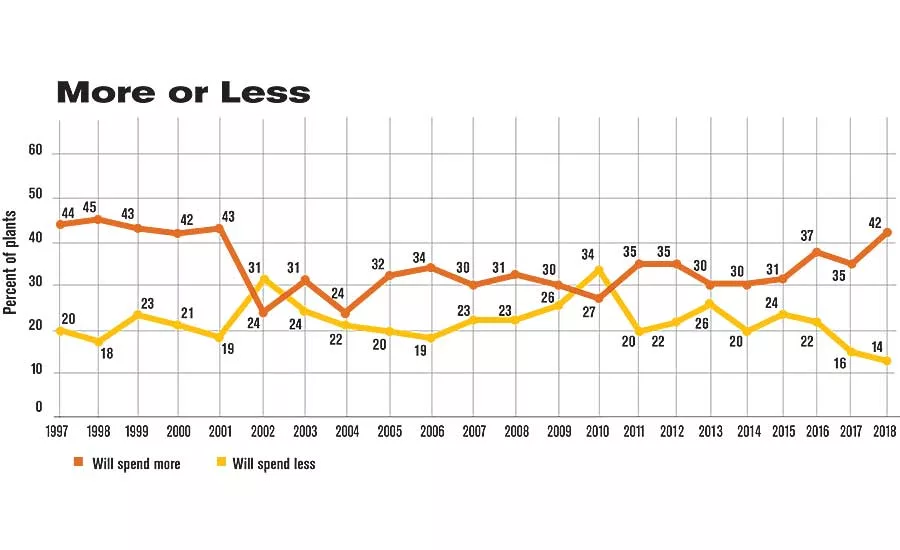

Some 42 percent of respondents will spend more on assembly technology next year than they did this year. That marks the eighth straight year that the “we’ll spend more” percentage has been above 30 percent, and it’s the highest such percentage since 2001.

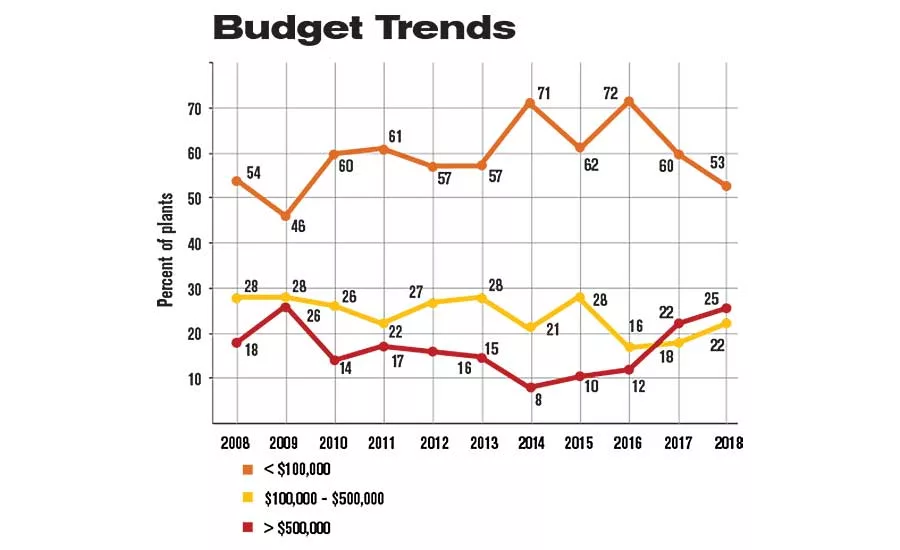

Aggregate budget data indicate a healthy increase in spending for 2018. For example, 25 percent of plants have capital budgets of at least $500,000. That’s the highest percentage since 2009.

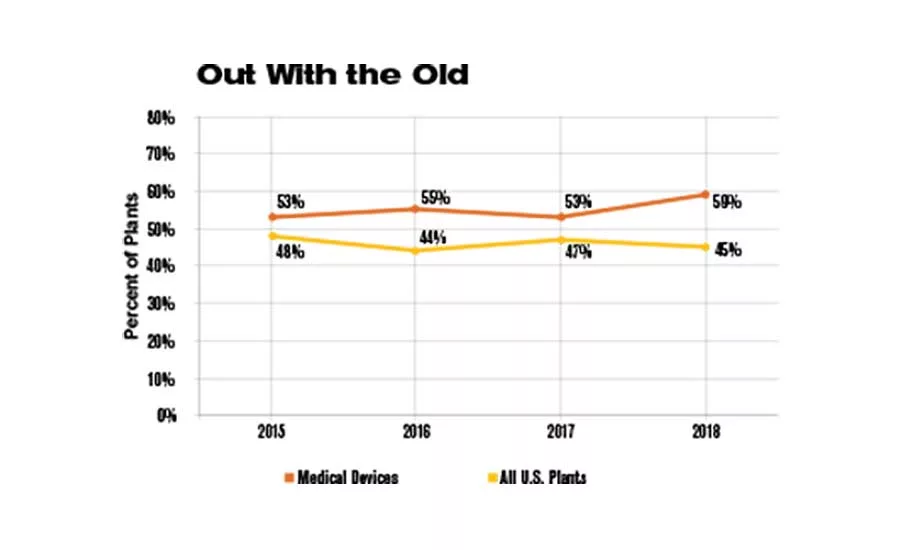

Compared with other industries, manufacturers of medical devices are more worried about aging machinery. Fifty-nine percent of plants in the medical device industry will buy equipment next year to replace old or worn-out equipment. That percentage has been above the national ratio for the past four years.

Only 29 percent of plants will buy equipment next year to assemble a new product. That’s the fifth time in the past six years in which that ratio has been below 30 percent.

Could U.S. assemblers be feeling pinched? Forty-seven percent of factories will buy equipment next year to increase capacity. That’s the highest since 2007.

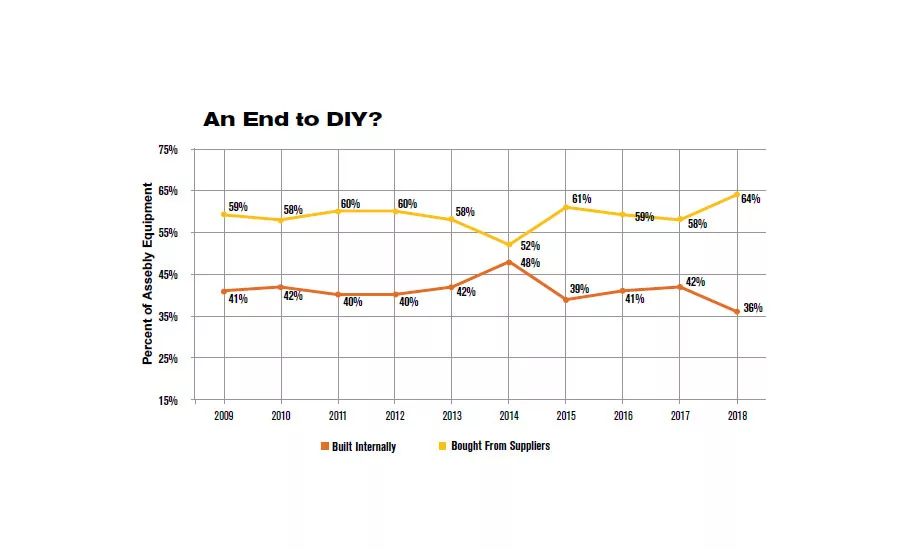

Assemblers are less and less interested in building their own assembly systems. Next year, engineers will fulfill, on average, just 36 percent of their system needs with equipment built in-house. That’s the lowest percentage in 19 years.

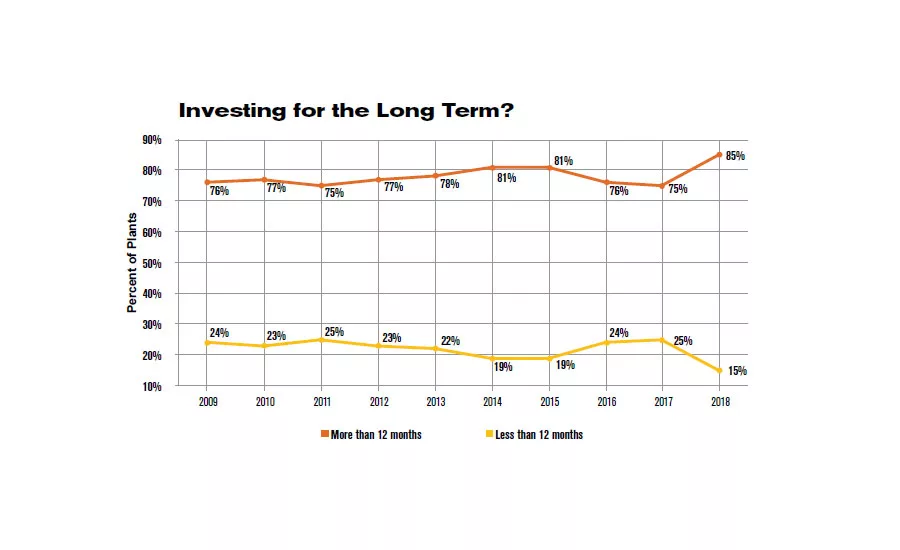

With the prospect of sustained, if modest, growth over the next few years, assemblers may be taking a longer term view on capital equipment investment. Next year, just 15 percent of plants have an ROI period of less than 12 months—the lowest percentage in survey history.

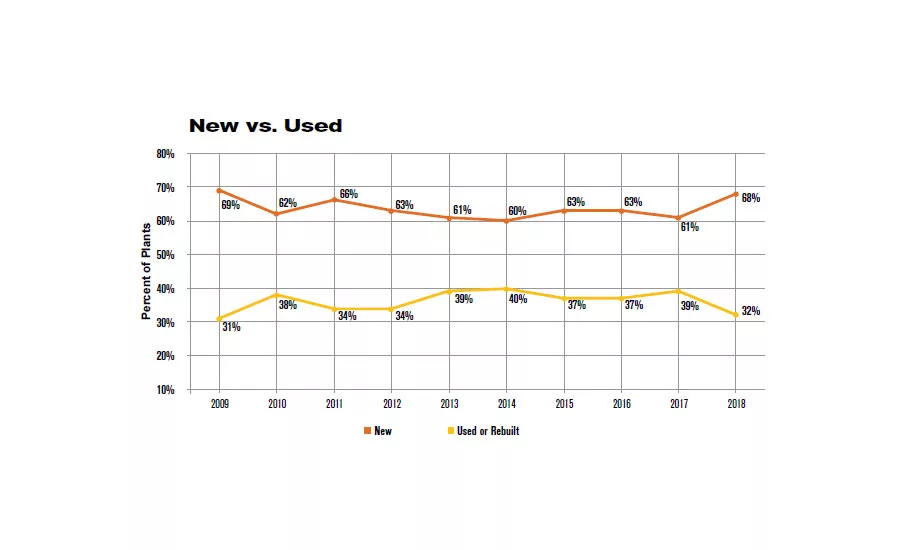

Given rapid advances in technology, used or rebuilt equipment may not be as popular as it once was. Next year, assemblers will allocate, on average, just 32 percent of their capital budgets to used equipment. That’s the lowest ratio in a decade.

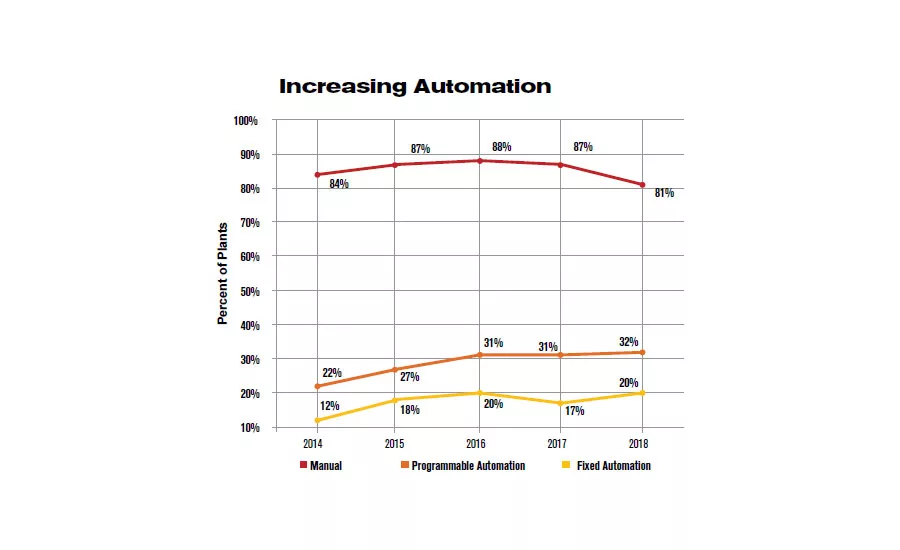

As more and more manufacturers bring work back from overseas, automation is becoming more important and manual assembly is decreasing.

U.S. manufacturing continued to roll in 2017. Want proof? Look no further than Toyota Motor Corp. In September, the world’s largest automaker announced that it will invest $374 million at five U.S. factories. Specifically, Toyota will spend:

- $106 million at its factory in Huntsville, AL, to build a new engine assembly line.

- $121 million to expand an engine assembly line in Georgetown, KY.

- $115 million to assemble hybrid vehicle transmissions in Buffalo, WV.

- $17 million to increase production of 2.5-liter cylinder heads in Troy, MO.

- $14.5 million to upgrade its factory in Jackson, TN, to accommodate production of transmission cases and engine blocks.

But wait—there’s more! In August, Toyota and rival Mazda Motor Corp. announced plans to build a $1.6 billion U.S assembly plant as part of a new joint venture. The plant will be capable of producing 300,000 vehicles a year, with production divided between the two automakers. The facility is expected to employ some 4,000 people when it opens in 2021.

Mazda, whose annual global vehicle sales are one-eighth that of Toyota, currently exports vehicles from Japan and Mexico to supply the U.S. market, where it generates roughly one-third of its global vehicle sales.

The factory is the first new automotive assembly plant to be announced during the tenure of President Donald Trump, who has pressured Toyota and other carmakers to make more of their vehicles in the U.S.

Alabama and North Carolina are the final states in the running to win the facility. The factory is such a hotly contested prize that Toyota and Mazda are pressing for an incentive package valued at $1 billion or more.

Such massive investment hasn’t only been confined to the automotive industry. Indeed, in every industry covered by ASSEMBLY magazine, manufacturers are investing in people, plants and equipment. Here are some of the manufacturing headlines from the past year:

- GKN Aerospace will invest $50 million to build a new assembly plant in Panama City, FL. The factory is expected to create 170 new jobs.

- Samsung Electronics will build a $380 million appliance assembly plant in Newberry, SC.

- Medical device manufacturer Baxter completed a $270 million expansion project that doubled the size of its assembly plant in Opelika, AL. The project will also double the facility’s workforce.

- Taiwanese electronics giant Foxconn plans to build a $10 billion plant in Wisconsin that will make liquid-crystal display panels and employ as many as 13,000 people.

The latest data from the Institute for Supply Management (ISM) provide further evidence that U.S. manufacturing is growing. The institute’s PMI index registered 58.7 percent in October, the 14th straight month that the index has exceeded 50 percent. A reading above 50 percent indicates that the manufacturing economy is generally expanding; below 50 percent indicates that it is generally contracting. Of the 18 manufacturing industries covered by the PMI, 16 reported growth in October.

Sales of machine tools also point to growth in U.S. manufacturing this year. According to AMT—The Association for Manufacturing Technology, sales of machining, stamping and forming equipment totaled $3.18 billion through the first nine months of 2017, a 5 percent increase from the same period last year. Similarly, sales of cutting tools totaled $1.637 billion for the first nine months of 2017, up 7 percent compared with the same period in 2016.

“While there is recovery in market conditions for manufacturing technology, it’s at a more gradual pace than typically seen due to a sentiment of caution around manufacturing,” says Doug Woods, AMT president. “Manufacturers are concerned about Washington’s impact on economic growth and the pace of technological change, as well as the general evolution in technology. It is necessary for companies to invest in current technologies to stay competitive, but they’re doing so at a moderate pace.”

Looking for quick answers on assembly and manufacturing topics? Try Ask ASM, our new smart AI search tool. Ask ASM

2017 also brought good news for manufacturers of appliances, furniture and construction equipment. U.S. home building jumped to a one-year high in October as disruptions caused by recent hurricanes in the South faded and communities in the region began replacing houses damaged by flooding.

Housing starts surged 13.7 percent to a seasonally adjusted annual rate of 1.29 million units, according to the Commerce Department. That was the highest level since October 2016. September’s sales pace was revised up to 1.135 million units from the previously reported 1.127 million units.

Groundbreaking activity in the South, which accounts for almost half of U.S. residential construction, plummeted in the aftermath of Hurricanes Harvey and Irma. The storms slammed Texas and Florida in late August and early September. However, housing starts in the South soared 17.2 percent in October to 621,000 units, with single-family construction vaulting 16.6 percent to its highest level since 2007. There were also increases in home building in the Midwest and Northeast.

Manufacturing employment more or less held steady this year. According to the latest figures from the Labor Department, U.S. manufacturers employed 12.48 million people through October 2017. That’s up a bit from the 12.32 million employed in October 2016, but it’s still more than 1 million more manufacturing jobs than there were in March 2010, the low point of the Great Recession.

Continued Growth

Will growth continue? The results of our 22nd annual Capital Equipment Spending Survey indicate that manufacturers will increase spending on assembly technology in 2018.

Specifically, U.S. assembly plants will spend $4 billion on new equipment in 2018, an increase of 6 percent from the $3.78 billion projected to be spent in 2017.

Some 42 percent of respondents will spend more on assembly technology next year than they did this year. That marks the eighth straight year that the “we’ll spend more” percentage has been above 30 percent, and it’s the highest such percentage since 2001. Forty-five percent will spend the same as they did in 2017, and only 14 percent of respondents will spend less in 2018 than they did 2017. The latter figure is an all-time low for our survey.

On average, manufacturers will spend $582,650 on assembly technology in 2018, more than twice the $273,108 average budget for 2017. The median budget figure is also up: from $50,000 in 2017 to $65,000 in 2018.

Aggregate budget data also indicate a healthy increase in spending for 2018. For example, 19 percent of plants have capital budgets of at least $1 million. That compares with 11 percent in 2017, and it’s the highest percentage since 1999. At the same time, 28 percent of plants will spend between $100,000 and $999,999 in 2018, virtually the same percentage as this year. Only 53 percent of plants will spend less than $100,000 next year. That compares with 60 percent in 2017, and it’s the lowest percentage in 10 years.

The aggregate budget data is all the more remarkable in that we received a slightly lower than normal response rate from the transportation equipment manufacturing industry, where we would expect to see increased capital spending. Similarly, we received a below-normal response rate from midsized assembly plants—9 percent vs. a 10-year average of 13 percent. Presumably, factories with 101 to 200 employees would have higher capital budgets than factories with fewer employees.

Nevertheless, our results seem to dovetail with other industrial forecasts. For example, according to the 2018 Metalworking Capital Spending Survey by Gardner Intelligence, U.S. metalworking facilities will spend $7.5 billion on new lathes, boring machines and other metal-cutting equipment next year, an increase of 5 percent from 2017. Gardner further predicts that spending on cutting tools will increase 15 percent, to $3.6 billion, next year.

The Manufacturers Alliance for Productivity and Innovation (MAPI) expects annual U.S. GDP growth to average 2.1 percent from 2017 to 2021. “While growth in the U.S. remains moderate and constrained by domestic political and policy challenges, there is no sign that the lengthy U.S. economic expansion, which began in June 2009, is about to end,” says Cliff Waldman, MAPI’s chief economist.

MAPI also predicts that growth in durable goods consumption will average 4.4 percent annually from 2017 to 2021, while growth in business equipment spending will average 3.8 percent. Overall, MAPI estimates that U.S. manufacturing will grow an average of 1.2 percent to 1.8 percent annually during the next five years.

With the prospect of sustained, if modest, growth over the next few years, assemblers may be taking a longer term view on capital equipment investment. Next year, just 15 percent of plants have a return on investment (ROI) period of less than 12 months—the lowest percentage in our survey’s history. At the same time, 36 percent of plants have an ROI period of at least two years. That’s the most since 2010.

Cost Cutting

For the first time since 2015, cost reduction is the No. 1 reason for investing in assembly technology. Some 47 percent of assembly plants are looking to lower costs in 2018. That compares with 44 percent in 2017 and 39 percent in 2016.

Cost reduction is particularly a concern among manufacturers of fabricated metal products. Fifty-five percent of fabricators are investing to reduce costs next year, marking the fourth straight year that this industry has been above the national figure.

Concern over cost reduction is typically related to the size of the product being assembled. For example, 69 percent of plants making products larger than a 6-foot cube will buy equipment to decrease production costs. That’s the highest percentage of any product size category, and it’s the fifth straight year large-product manufacturers have been above the national ratio.

That makes sense. Cars, tractors, jets and other products larger than a 6-foot cube are more expensive, of course, but, ironically, they are often more price-sensitive. Such products have more components and thus, offer more opportunities for cost reduction. Very large products are also more labor-intensive to assemble, and their production processes are more difficult to automate.

Conversely, small-product assemblers are much less concerned about cost reduction. Only 36 percent of plants making products smaller than a 12-inch cube will buy equipment to decrease production costs. That’s the lowest percentage of any product size category, and it’s the second straight year small-product manufacturers have been below the national ratio.

That makes sense, too, since it’s more difficult to lower the cost of assembling syringes, for example, than it is to reduce the cost of making motorcycles. What’s more, small products tend to be assembled on automated lines. Indeed, 29 percent of small-product assemblers employ fixed automation at their facilities, vs. 17 percent for all U.S. plants.

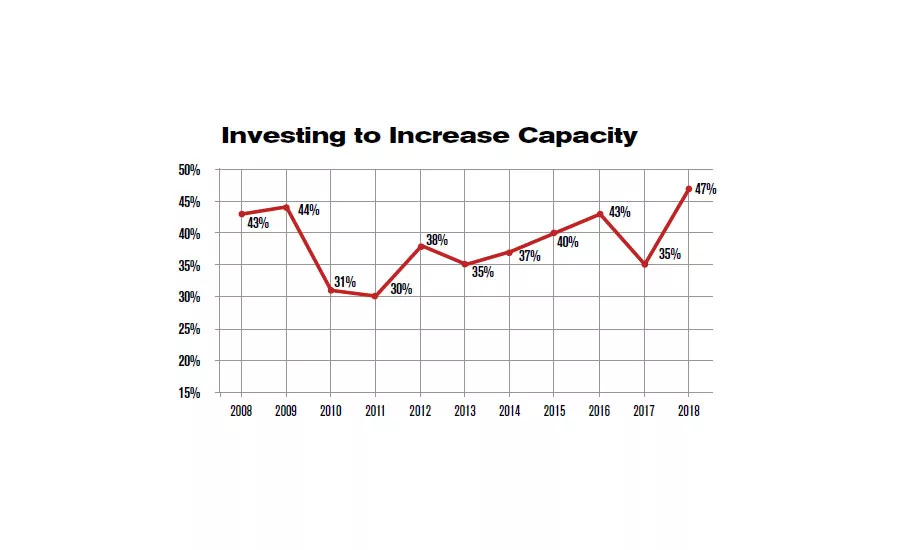

Increasing Capacity

According to latest figures from the Federal Reserve, U.S. manufacturing operations were running at 76.4 percent of capacity in October, an increase of 1.4 percentage points from October 2016. That’s still well below the high-water mark of 85.6 percent set in 1989, but it’s inching closer to the 44-year average of 78.4 percent.

Could U.S. assemblers be feeling pinched? Perhaps. Forty-seven percent of U.S. assembly plants will buy equipment next year to increase capacity or assemble higher volumes of existing products. That compares with 35 percent in 2017, and it’s the highest since 2007.

The need for more capacity is particularly acute among medical device manufacturers. Some 52 percent of plants—more than any other industry—are investing in equipment to boost capacity. It’s the fourth time in five years that that figure has been above 42 percent.

On the other hand, manufacturers of fabricated metal products seem to have plenty of capacity. Only 20 percent of plants in this industry will buy equipment next year to increase capacity. That’s well below the national percentage, and it’s an all-time low for this industry. In fact, the fabricated metal products industry has been below the national percentage for the past seven years.

One might think that smaller companies would be more likely to increase capacity than larger ones, but in fact, the opposite is true. Just 33 percent of factories with 20 employees or less will buy equipment next year to increase capacity. That compares with 56 percent of plants with 21 to 100 employees; 73 percent of plants with 101 to 200 employees; and 50 percent of plants with more than 200 employees. A similar pattern can be seen in the data for the past five years.

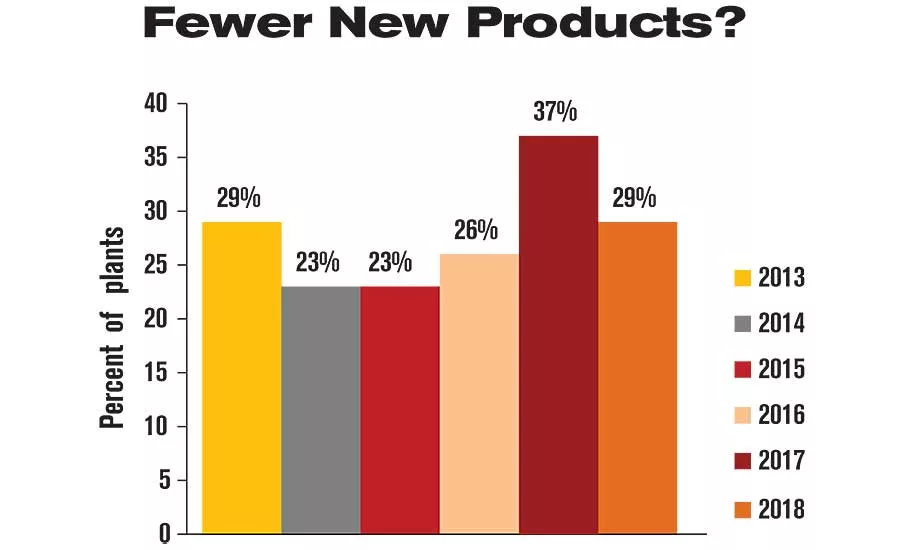

Fewer New Products?

Only 29 percent of plants will buy equipment next year to assemble a new product. That compares with 37 percent in 2017, and it marks the fifth time in the past six years in which that ratio has been below 30 percent. Historically, that figure has averaged 38 percent.

Oddly, 55 percent of plants in the fabricated metal products industry will buy equipment next year to assemble a new product. That’s the most of any industry, and it’s the third straight year that fabricators have held that distinction. However, that high percentage may be more of a reflection of the nature of the business than an influx of truly new products.

As one might expect, 43 percent of medical device manufacturers and 37 percent of electronics manufacturers are investing in technology to assemble new products, but only 13 percent of appliance and electrical equipment manufacturers are doing so. The latter percentage is the lowest of any industry, and it marks the third straight year that appliance and electrical equipment manufacturers have been on the bottom in that regard.

Get it Out the Door!

Thirty-five percent of plants will buy equipment in 2018 to reduce cycle time or eliminate a bottleneck. That compares with 31 percent in 2017, and it’s the most since 2011.

Machinery manufacturers are particularly keen to get their products out the door quicker. Almost half (48 percent) of plants in this industry will invest in technology next year to reduce cycle time. In fact, the industry has been above the national figure for five of the past six years.

Other motives for buying equipment include:

- replace old or worn-out equipment, 45 percent.

- implement lean manufacturing, 23 percent.

- increase safety, 23 percent.

- increase quality, 15 percent.

- keep up with competition, 13 percent.

- meet OEM or downstream requirements, 11 percent.

- comply with standards or industry regulations, 11 percent.

Labor Costs

As always, the top two targets for cost reduction are direct labor and indirect labor. However, with the unemployment rate at 4.5 percent and predictions that as many as 2 million manufacturing jobs might go unfilled over the next decade, manufacturers may be getting more concerned about labor costs.

Some 77 percent of plants are looking to decrease direct labor costs next year. That compares with 72 percent in 2017, and it’s the highest percentage since 2012. Similarly, 40 percent of plants hope to lower indirect labor costs, such as setup and maintenance. While that is down from 49 percent in 2017, that ratio was in the thirties from 2013 to 2016.

Whether concern over direct and indirect labor costs are justified remains to be seen. Up to now, wage growth in manufacturing has essentially been flat. According to the Bureau Labor Statistics, wages for U.S. manufacturing workers have increased just 2 percent, from an average of $20.61 per hour in October 2016 to $21.06 per hour in October 2017. That’s well short of the Federal Reserve’s target of 3.5 to 4 percent for nominal wage growth (assuming 2 percent inflation target, 1.5 percent productivity growth, and a stable labor share of income).

However, wages for U.S. manufacturing workers are projected to rise 4 percent, to an average of $21.87 per hour in October 2018, and they could increase to as much as $25.61 per hour by 2020.

One industry that is not concerned about direct labor costs is medical device manufacturing. Only 57 percent of plants in that industry are targeting direct labor costs next year, marking the fourth straight year that this industry has been below the national figure. That makes sense. Medical devices tend to be small, high-value products produced at high volumes, which makes them ideal candidates for automated assembly.

Larger facilities are typically more concerned about labor costs that smaller ones. For example, 84 percent of plants with more than 200 workers and 87 percent of plants with 101 to 200 employees are looking to reduce direct labor costs next year. That compares with 71 percent of plants with 20 workers or less and 72 percent of plants with 21 to 100 workers.

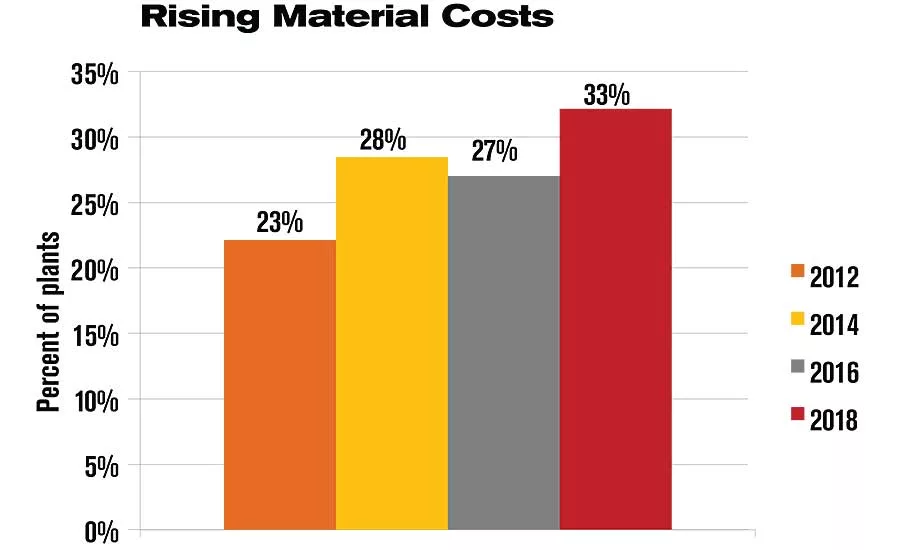

Rising Material Costs

As manufacturers increase their consumption of exotic materials, such as composites and titanium, a growing number are concerned over the cost of those materials. Thirty-three percent of assembly plants are looking to lower material costs next year. That’s a record high, and it’s the sixth straight year in which that percentage has been 25 percent or more.

Material costs are particularly concerning to manufacturers of medical devices and electrical equipment and appliances. In fact, material costs have been a concern for 30 percent or more of medical device assemblers for five consecutive years.

Not surprisingly, manufacturers of large products are more concerned about material costs than manufacturers of smaller ones. Some 39 percent of plants making products larger than a 6-foot cube and 41 percent of plants making products larger than a 3-foot cube will be targeting material costs. In contrast, only 24 percent of factories assembling products smaller than a 12-inch cube will do so.

Crack That WIP

There’s little doubt that lean manufacturing has made a tremendous impact on assembly plants over the years—and it still is. Indeed, 23 percent of plants will purchase equipment next year to implement lean, up from 16 percent in 2017.

The fruits of those efforts are reflected in the costs assemblers are targeting—or rather, not targeting—in the coming year. For example, in 1998, 36 percent of plants were looking to reduce the cost of work-in-process inventory—one of the “seven wastes” of lean. Next year, only 14 percent of plants will do so. In fact, that percentage has not exceeded 20 percent in seven years.

Similarly, assemblers have done a great job reducing defects, another of the seven wastes (automotive recalls notwithstanding). Only 8 percent of assemblers are hoping to reduce warranty costs in the coming year, which ties the record low for our survey. In fact, from 1997 to 2001, an average of 17 percent of plants wanted to reduce warranty costs. But, from 2014 to 2018, only 10 percent of plants, on average, were targeting warranty costs.

Other targets for cost reduction include:

- Scrap and rework, 38 percent.

- Energy costs, 16 percent.

What Assemblers Want

As usual, power tools will be the No. 1 item on assemblers’ shopping lists next year, though demand may not be as strong as in previous years. Some 55 percent of assembly plants will purchase impact wrenches, cordless screwdrivers, DC electric nutrunners, handheld riveters and other power tools in 2018. That compares with 68 percent in 2017, and it’s the lowest percentage since 2013. Demand will be particularly strong among medical device manufacturers and appliance assemblers.

All totaled, assemblers will spend $230 million on tools next year, or 2 percent less than they spent in 2017.

Another technology that should enjoy an increase in demand is conveyors and material handling equipment. A whopping 40 percent of plants will buy such equipment in 2018. That compares with 25 percent in 2017, and it ties the record-high percentage set way back in 1998. Demand will be highest among manufacturers of medical devices, appliances and machinery.

“I would definitely expect conveyor sales to increase in U.S. assembly plants,” says Joe Ambrose, marketing manager for FlexLink Systems Inc. “For FlexLink, our classic conveyor systems and workstations are always a great choice, but in addition, we have developed new solutions for assembly plants. At The Assembly Show, we introduced our twin-track conveyor for heavy products. It was well-received by many of our booth visitors.

“With record numbers of quality attendees and leads at trade shows in 2017, and with so many companies building new plants or revamping existing ones, we will likely see sales continuing to increase in 2018. I believe it follows suit with your findings.”

All totaled, spending on conveyors and material handling equipment should increase 32 percent, from $75.6 million in 2017 to $100 million in 2017.

Our survey results also indicate a strong increase in demand for robots. Nineteen percent of plants will purchase robots next year, the most since 2015. All totaled, assemblers will spend $252.9 million on six-axis robots, SCARAs, grippers and other robotic technology next year, an increase of 41 percent over 2017 sales.

Such an increase is not hard to imagine given what’s already happened this year. According to the Robotics Industries Association, the North American robotics market had its best opening half ever to begin 2017, setting new records in all four statistical categories (order units, order revenue, shipment units, and shipment revenue). In total, 19,331 robots valued at approximately $1.031 billion were sold in North America during the first six months of 2017. These figures represent growth of 33 percent in units and 26 percent in dollars over 2016. Automotive-related orders grew substantially in that time, increasing 39 percent in units and 37 percent in dollars, while non-automotive orders also grew 21 percent in units and 10 percent in dollars over the first half of 2016.

Suppliers of automatic screwdriving equipment could see their sales rise next year. Some 29 percent of plants will buy automatic screwdriving equipment next year. That compares with 27 percent in 2017, and it’s the highest percentage since 2011. Demand will be strongest in the machinery, transportation equipment, and medical device industries.

In all, assemblers will spend $231 million on automatic screwdriving equipment next year, and increase of 18 percent over 2017.

The biggest decrease in demand will be for inspection equipment. Although 52 percent of assemblers plan to purchase vision systems, sensors and other inspection technologies next year—a record high for our survey—they are allocating fewer dollars for the technology. All totaled, sales of inspection equipment will decrease 5 percent, from $241.7 million in 2017 to $230 million in 2018.

The biggest markets for inspection technology next year will be makers of machinery, computers and electronics, transportation equipment, and appliances.

Please visit www.clearmarkettrends.com to purchase and download the entire report, as well as access a wide inventory of other studies done in this industry. You can also email info@clearmarkettrends.com with any questions.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!