Tipping point?

Battery electric vehicles could be on the fast track to reach an installed base of over 100 million by 2029, but much of the growth in electrification hinges on battery technology as well as educated and willing consumers.

The electrification of automotive powertrains has accelerated as the world’s automakers come to the realization that traditional ICE (internal combustion engine) vehicles can no longer keep pace with stringent global emissions requirements, especially those in Europe. These tightening global regulations are paving the way for BEV (battery electric vehicle) sales to grow from 1.3% in 2018 to 16.4% in 2029, creating an electric vehicle (EV) installed base of more than 100 million, forecasts global tech market advisory firm, ABI Research.

“Simultaneously, automakers are seeking to alleviate consumer fears about EV range by rapidly increasing battery capacity, using new battery technologies, such as silicon-dominant anodes and solid-state designs, to increase cell-level energy density from 250 W·h/kg to more than 500 W·h/kg within the next 10 years,” said James Hodgson, Principal Analyst at ABI Research.

The expected growth in EVs and the energy density of their batteries represent a considerable challenge to the energy industry, with energy demand for electric passenger vehicles expected to grow from 1121 GW·h in 2018 to 19,141 GW·h in 10 years.

“While this represents a potential of almost $20 billion in energy sales by 2028, it also places extraordinary demands on national energy grids, with Transmission System Operators (TSOs) struggling to accommodate the onboarding of BEVs due to the limitations in infrastructure at the last mile, particularly with line constraints, transformer limitations, and the syncing of renewable energy supply with usage,” says Hodgson.

These factors have opened a market opportunity for smart energy management companies to support TSOs in the onboarding of EVs, incentivizing consumers via rewards and revenue sharing to encourage charging during off-peak hours. Potential benefits include helping TSOs to strategically improve last-mile infrastructure without impeding EV adoption and helping energy retailers to better predict energy demand to avoid demand charges.

Capacity building

Tradition and new mobility vehicle makers are responding to the need for cleaner solutions with EV production capacity.

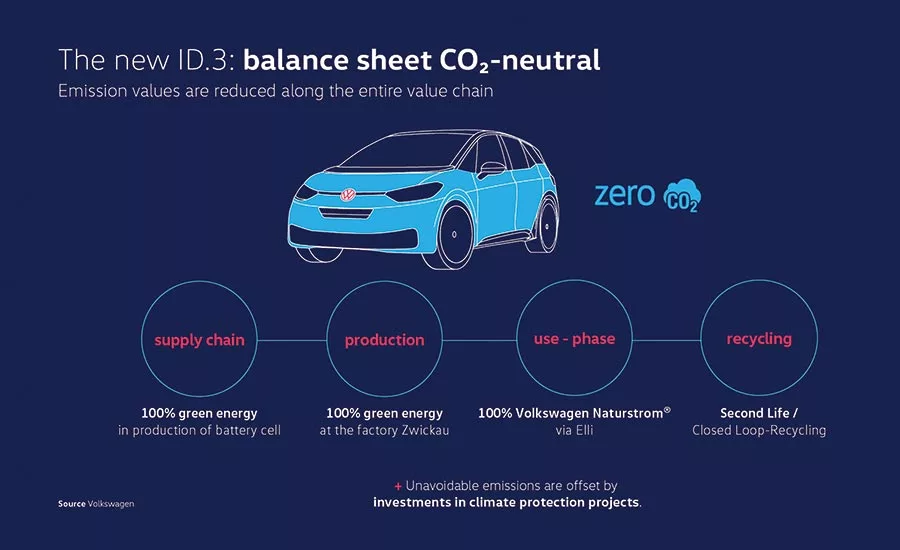

In November, industry behemoth Volkswagen initiated its big changeover to e-mobility, with production starting in Zwickau, Germany on the first car in the company’s new generation of electric vehicles—a white ID.3. The importance of the launch was punctuated by an assembly line watched by Federal Chancellor Dr. Angela Merkel and Group CEO Dr. Herbert Diess.

Looking for quick answers on assembly and manufacturing topics? Try Ask ASM, our new smart AI search tool. Ask ASM

The Volkswagen Group plans to sell some 22 million EVs worldwide by 2028. Zwickau has a key role to play, the large car manufacturing plant being entirely converted to e-mobility backed with investments currently at €1.2 billion. Plans call for 2020 production of some 100,000 electric models and eventually up to 330,000 EVs—making the site the largest and most efficient EV factory in Europe, according to Volkswagen.

The ID.3 is based on Volkswagen’s Modular Electric Drive Toolkit (MEB), an all-electric platform aimed at fully leveraging the opportunities offered by e-mobility. It is said to set “new benchmarks in sustainability,” with production said to be carbon neutral. In the final expansion stage from 2021, six MEB models from three Volkswagen Group brands will be built in Zwickau.

At the other end of the OEM-size spectrum, startup Lucid Motors began construction at its first EV factory in Arizona where its first EV, the Lucid Air luxury sedan, will be assembled. The first phase of factory construction, in Casa Grande, AZ, represents an investment of more than $300 million and is scheduled for completion in late 2020 in readiness for the start of production of the U.S. designed and engineered car.

“The Lucid Air is a cutting-edge electric vehicle designed, engineered, and destined for manufacture entirely in America,” said Peter Rawlinson, CEO and CTO, Lucid Motors. “With supportive investors, an outstanding team of designers and engineers, and a product strategy that extends well beyond the Air.”

The factory is expected to have a positive economic impact on the city, county, and state with 4800 direct and indirect jobs by 2029; over $700 million in capital investment by Lucid by the mid-2020s; and an estimated $32 billion revenue impact for the city and county over a 20-year period.

Battery backup

Of course, all of the EV-assembly investments will depend on a supporting ramp-up in battery production. Increased EV volumes have already brought greater demand and economies of scale to the battery industry, but further improvements are needed.

Battery prices, which were above $1100/kW·h in 2010, have fallen 87% in real terms to $156/kW·h in 2019, according to research company BloombergNEF (BNEF). By 2023, its latest forecasts project that average prices will be close to $100/kW·h—the price seen as the point around which EVs start to reach price parity with ICE vehicles.

The cost reductions in 2019 were thanks to increasing order size, growth in battery electric vehicle sales, and the continued penetration of high energy density cathodes. The introduction of new pack designs and falling manufacturing costs will drive prices down in the near term. BNEF’s 2019 Battery Price Survey published in December predicts that, as cumulative demand passes 2 TW·h in 2024, prices will fall below $100/kW·h.

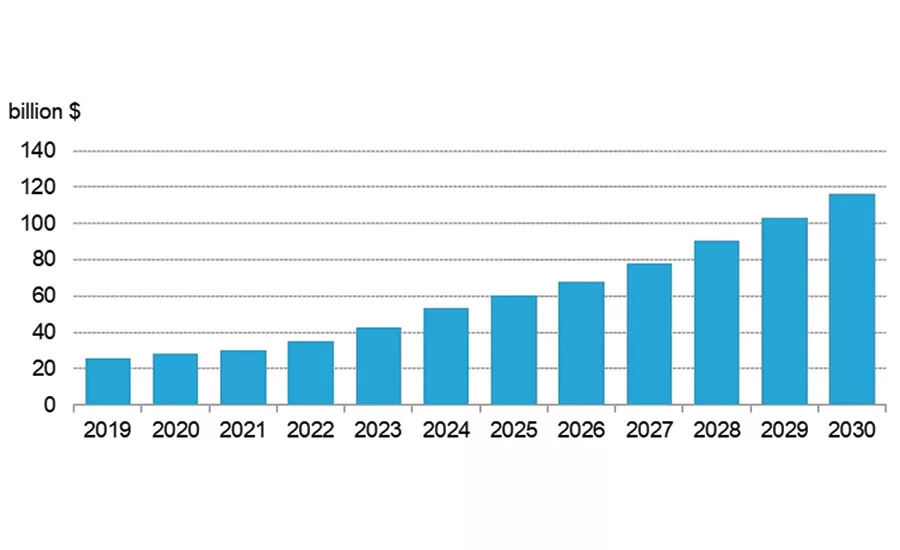

“According to our forecasts, by 2030 the battery market will be worth $116 billion annually, and this doesn’t include investment in the supply chain,” said James Frith, BNEF’s senior energy storage analyst and author of the report. “However, as cell and pack prices are falling, purchasers will get more value for their money than they do today.”

BNEF’s analysis finds that, as batteries become cheaper, more sectors are electrifying. For example, electrification of commercial vehicles, such as delivery vans, is becoming increasingly attractive. This will lead to further differentiation in cell specifications, with commercial and high-end passenger vehicle applications likely to opt for metrics like cycle life over continued price declines. However, for mass-market passenger EVs, low battery prices will remain the most critical goal.

While the path to achieving $100/kW·h by 2024 looks promising, BNEF experts believe there is much less certainty on how the industry will reduce prices further—perhaps down to $61/kW·h by 2030—because there are a variety of options and paths that can be taken. In the second half of the 2020s, energy density at the cell and pack level will play a growing role as it allows for more efficient use of materials and manufacturing capacity. New technologies like silicon or lithium anodes, solid-state cells, and new cathode materials will be key to helping cost reductions play out.

Consumer experience upgrade

While the production volumes will be there, its where the EV rubber meets the road at dealerships that could make or break consumer demand. The consumer will have to be served better, if anecdotal and survey evidence is to be believed.

A new Sierra Club report shows that the U.S. auto industry is largely failing to meet consumer demand for EVs. Based on surveys from 579 volunteers who called or visited 909 different auto dealerships and stores across all 50 states to inquire about EVs, the study found that dealerships and automakers have massive room for improvement to increase EV availability, make sure that EVs are prominently displayed and charged for test drives, and ensure that salespersons are offering important information upfront about charging, range, and consumer incentives like federal and state financial incentives.

The report reveals that 74% of auto dealerships nationwide aren’t selling electric vehicles. Furthermore, in 28% of dealerships visited, salespeople provided no information at all about how to charge an EV, and in 31% of dealerships visited, salespeople did not provide any information on state and federal incentives.

When volunteers asked to test drive an EV, the vehicle was insufficiently charged and unable to be driven 10% of the time. Of the dealerships that sold EVs, more than 66% did not display EVs prominently, with vehicles sometimes buried far in the back.

Among automakers, Tesla was reported as providing the best consumer shopping experience, with an average satisfaction score of 4.5 out of 5, and Chrysler was reported as providing the worst consumer shopping experience, with an average satisfaction score of 2.9 out of 5.

“The auto industry needs to end its greenwashing claim that it’s committed to an electric future when, in reality, automakers and dealerships are dragging their feet to offer consumers the electric vehicles they want and deserve,” said Hieu Le, a campaign representative with the Sierra Club’s Clean Transportation for All campaign and the main author of the report. “It’s past time for the auto industry to put some action behind its promises of progress and work to tackle emissions from transportation.”

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!